Dear visitor

You tried to access but this page is only available for

You tried to access but this page is only available for

Witold Bahrke

Senior Macro and Allocation Strategist

Why has the consensus proven wrong?

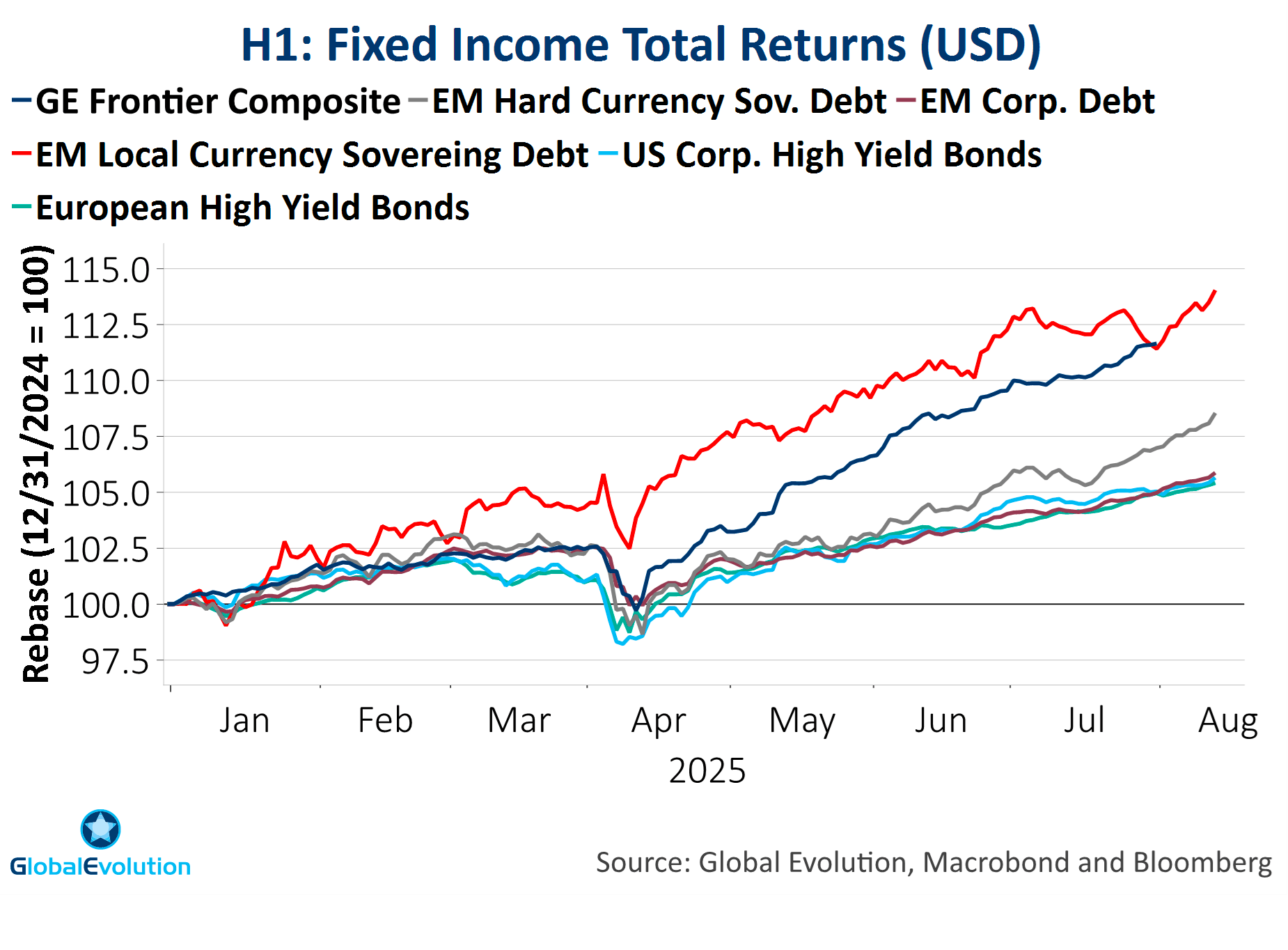

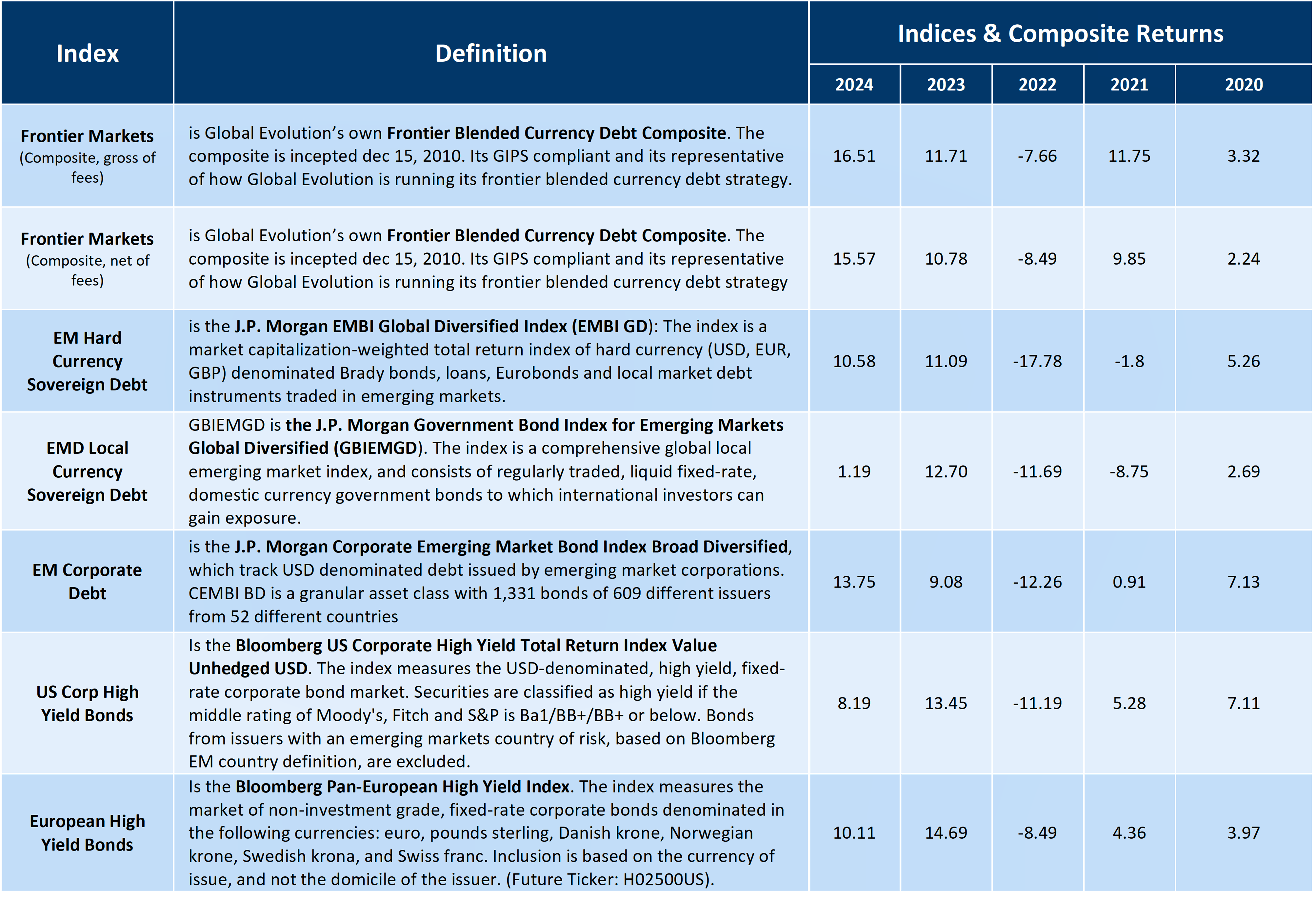

Investors find themselves in a world where uncertainties abound. Nevertheless, Emerging Market bonds have shown remarkable resilience year-to-date, proving the consensus at the beginning of the year spectacularly wrong. Neither elevated trade policy uncertainty nor mounting geopolitical risks have done much harm to emerging market debt (EMD). Not only are returns comfortably in positive territory. The asset class also managed to outperform its DM peers such as US High Yield bonds (see Chart 1). EM sovereign bonds issued in local currencies are topping the list with double digit returns in the first half of the year (please refer to table 1 for clarification of indices).

For investors, this begs the question whether this is a one off. We don’t think it’s a lucky punch, but more deeply rooted as the structural drivers behind a more uncertain investment landscape originate in the developed world, not in EM. This is not to say the EM assets are immune to rising uncertainties of various kinds, but they do not stand first in line when it comes to the negative spillovers and might even be able to benefit from higher uncertainty. In our view, the correct narrative therefore is that EMD has outperformed because of a more uncertain investment environment – not despite of it. So what are the primary structural drivers behind rising uncertainty? We believe it mainly comes down to three regime shifts, the world economy is currently undergoing.

Three regime shifts

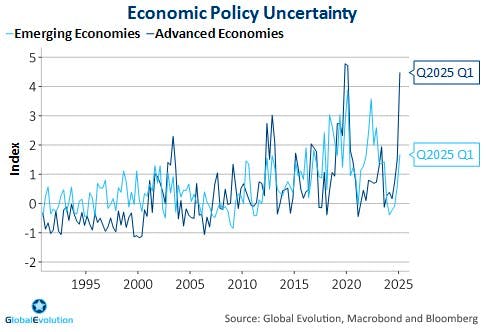

First, investors grapple with a structural shift towards higher policy uncertainty and geopolitical risks. Uncertainty is rarely positive for risk appetite, neither in EM nor DM. However, it’s worth keeping in mind that various measures of policy uncertainty have risen much more in developed markets – first and foremost in the US – than in the emerging world[1] (see Chart 2). This goes both for economic policy as such, and trade policy, in particular. While we believe the shift towards higher geopolitical and policy uncertainty marks a regime shift for the global economy overall, it appears to be driven out of developed market, supporting the relative performance of EM bonds.

These types of uncertainties are unlikely to return to pre-pandemic levels anytime soon. On a positive note, however, the latest trade policy twist and turns confirm our view that policy uncertainty peaked around “liberation day” in early April, which should buoy overall risk appetite going forward. The mirror image of peak policy uncertainty is a convergence of the effective US tariff rate below recessionary levels (around 20% in our view) over the coming months, supporting the absolute performance of EM debt, as well. In line with our main scenario for Trump’s second term (see here), the US administration has “blinked” several times in the tariff game of chicken, postponing deadlines and at least partially backtracking from previously announced tariff rates. When push comes to shove, President Trump seems unwilling to accept the recession risks stemming from an effective tariff rate of around 25% as it stood in early April, when uncertainty peaked.

Still, geopolitical risks and policy uncertainty are likely to remain above their historical averages, albeit below the extreme levels seen in March and April. The tariff genie is out of the bottle. Hoping for a return to 2024 tariff levels seems futile. Contrary to what one might expect, our analysis shows that such an environment of high, but not extreme policy uncertainty is supportive for EM debt returns, even in absolute terms, see 3 Questions for EM Investors - Part II. What might seem counterintuitive, can probably be explained by some kind of central bank easing that tends to follow episodes of heightened policy uncertainty – exactly the type of easing the market is currently expecting with one full percentage point of cuts from the US central bank priced in the coming 12 months.

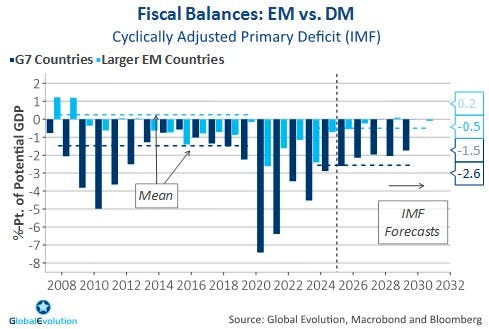

Secondly, we are currently witnessing a regime shift from fiscal conservatism to fiscal largesse, fueling uncertainty around countries’ debt trajectory and credit worthiness, in and of itself a key driver of global bond markets. As with geopolitical risks and policy uncertainty, this regime shift is mostly a developed markets phenomenon. Budget deficits adjusted for cyclical effects are set to perform worse in DM than in EM over the coming years (see Chart 3). Politicians in emerging markets have learned some of their lessons from previous episodes of fiscal risks spiraling out of control. DM policymakers, on the other hand, show no appetite for fiscal discipline. The current tax package negotiated in the US congress and Germany’s quantum leap towards higher defense and infrastructure spending are testament to this. In the wake of structurally higher DM deficits, investors naturally demand a higher compensation for fiscal risks in the form of higher yields (i.e. a lower price for bonds) – more so in DM than in EM. While this is not the only factor explaining a tightening of the EM-DM yield gap since the onset of the pandemic, it certainly contributed, benefitting the relative performance of EM debt versus DM debt.

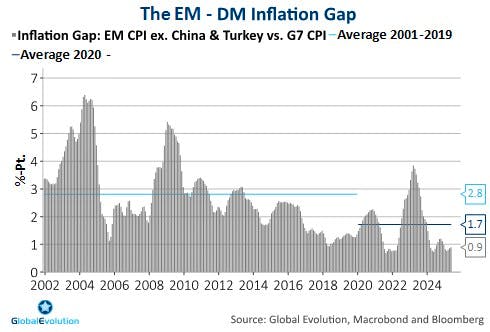

Thirdly, the transition from a low inflation environment to a somewhat higher trend inflation is primarily a DM story, as well. In Developed Markets, geopolitical risks, the changing contours of globalization, newfound fiscal largesse as well as demographics caused an exit from the post-GFC “low-flation” era. In the Emerging Markets sphere, however, a relatively disciplined monetary and fiscal policy stance and dis-inflationary forces from China has prevented trend inflation from rising (see EM Inflation: mind the gap).

Developed economies leaving the low-flation era behind means the trade-off between growth and inflation is deteriorating. Going forward, accelerating growth will create higher inflation risks as compared to the pre-pandemic years. Consequently, inflation uncertainty is rising. Again, investors need compensation for higher inflation risks, which comes in the shape of higher yields. On the EM side of the equation, there are limited signs of a deteriorating growth-inflation trade-off as inflation today is by-and-large where it was before the pandemic, lending additional support to the relative performance of EM debt. We believe the gap between EM and DM inflation has narrowed not only cyclically, but structurally. Such a regime shift should improve the risk-reward in EM debt relative to DM bonds. Particularly local currency debt stands to benefit as lower inflation means higher real rates, supporting EM currencies.

EMD resilience: Rethinking the narrative

The bottom-line is that some of the most prominent regime shifts causing a more uncertain macro and market environment are a bigger challenge for developed markets than for emerging markets. This is not least a reflection of improving policy credibility as well as macro stability in Emerging Markets over recent years. Current accounts are back in positive territory and external debt levels have declined substantially from 2020-highs. It goes without saying that emerging market debt returns aren’t immune to higher policy uncertainty, whether it originates in EM or DM countries. Higher DM yields resulting from elevated inflation and fiscal uncertainty will not go unnoticed in EM, either, as these yields are key drivers of global monetary conditions. However, the key point here is that emerging markets are not first in line to be challenged by these factors and might even benefit from them. In the same vein, higher uncertainty and strong EMD performance do not contradict each other, forcing many investors to rethink the market narrative. The DM-centric nature of the structural drivers behind a more uncertain investment environment implies that the resilience of EM debt is a feature, not a fluke.

[1] See e.g. http://www.policyuncertainty.com.

Disclaimer & Important Disclosures

Global Evolution Asset Management A/S (“GEAM”) is incorporated in Denmark and authorized and regulated by the Danish FSA (Finanstilsynet). GEAM DK is located at Buen 11, 2nd Floor, Kolding 6000, Denmark.

GEAM has a United Kingdom branch (“Global Evolution Asset Management A/S (London Branch)”) located at Level 8, 24 Monument Street, London, EC3R 8AJ, United Kingdom. This branch is authorized and regulated by the Financial Conduct Authority under FCA # 954331. In Canada, while GEAM has no physical place of business, it has filed to claim the international dealer exemption and international adviser exemption in Alberta, British Columbia, Ontario, Quebec and Saskatchewan.

In the United States, investment advisory services are offered through Global Evolution USA, LLC (‘Global Evolution USA”), a Securities and Exchange Commission (“SEC”) registered investment advisor. Global Evolution USA is located at: 250 Park Avenue, 15th floor, New York, NY. Global Evolution USA is a wholly owned subsidiary of Global Evolution Financial ApS, the holding company of GEAM. Portfolio management and investment advisory services are provided to GE USA clients by GEAM. GEAM is exempt from SEC registration as a “participating affiliate” of Global Evolution USA as that term is used in relief granted by the staff of the SEC allowing U.S. registered investment advisers to use investment advisory resources of non-U.S. investment adviser affiliates subject to the regulatory supervision of the U.S. registered investment adviser. Registration with the SEC does not imply any level of skill or expertise. Prior to making any investment, an investor should read all disclosure and other documents associated with such investment including Global Evolution’s Form ADV which can be found at https://adviserinfo.sec.gov.

In Singapore, Global Evolution Fund Management Singapore Pte. Ltd (“Global Evolution Singapore”) has a Capital Markets Services license issued by the Monetary Authority of Singapore for fund management activities. It is located at Level 39, Marina Bay Financial Centre Tower 2, 10 Marina Boulevard, Singapore 018983.

GEAM, Global Evolution USA, and Global Evolution Singapore, together with their holding companies, Global Evolution Financial Aps and Global Evolution Holding Aps, make up the Global Evolution group affiliates (“Global Evolution”).

Global Evolution, Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC, and Pearlmark Real Estate, L.L.C. and its subsidiaries are all direct or indirect subsidiaries of Conning Holdings Limited (collectively, “Conning”) which is one of the family of companies whose controlling shareholder is Generali Investments Holding S.p.A. (“GIH”) a company headquartered in Italy. Assicurazioni Generali S.p.A. is the ultimate controlling parent of all GIH subsidiaries. Conning has investment centers in Asia, Europe and North America.

Conning, Inc., Conning Investment Products, Inc., Goodwin Capital Advisers, Inc., Octagon Credit Investors, LLC, PREP Investment Advisers, L.L.C. and Global Evolution USA, LLC are registered with the SEC under the Investment Advisers Act of 1940 and have noticed other jurisdictions they are conducting securities advisory business when required by law. In any other jurisdictions where they have not provided notice and are not exempt or excluded from those laws, they cannot transact business as an investment adviser and may not be able to respond to individual inquiries if the response could potentially lead to a transaction in securities.

Conning, Inc. is also registered with the National Futures Association. Conning Investment Products, Inc. is also registered with the Ontario Securities Commission. Conning Asset Management Limited is Authorised and regulated by the United Kingdom's Financial Conduct Authority (FCA#189316); Conning Asia Pacific Limited is regulated by Hong Kong’s Securities and Futures Commission for Types 1, 4 and 9 regulated activities; Global Evolution Asset Management A/S is regulated by Finanstilsynet (the Danish FSA) (FSA #8193); Global Evolution Asset Management A/S (London Branch) is regulated by the United Kingdom's Financial Conduct Authority (FCA# 954331); Global Evolution Asset Management A/S, Luxembourg branch, registered with the Luxembourg Company Register as the Luxembourg branch(es) of Global Evolution Asset Management A/S under the reference B287058. It is also registered with the CSSF under the license number S00009438. Conning primarily provides asset management services for third-party assets.

This publication is for informational purposes and is not intended as an offer to purchase any security. Nothing contained in this communication constitutes or forms part of any offer to sell or buy an investment, or any solicitation of such an offer in any jurisdiction in which such offer or solicitation would be unlawful.

All investments entail risk, and you could lose all or a substantial amount of your investment. Past performance is not indicative of future results which may differ materially from past performance. The strategies presented herein invest in foreign securities which involve volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging and frontier markets. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, and credit.

While reasonable care has been taken to ensure that the information herein is factually correct, Global Evolution makes no representation or guarantee as to its accuracy or completeness. The information herein is subject to change without notice. Certain information contained herein has been provided by third party sources which are believed to be reliable, but accuracy and completeness cannot be guaranteed. Global Evolution does not guarantee the accuracy of information obtained from third party/other sources.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

Legal Disclaimer ©2025 Global Evolution.

This document is copyrighted with all rights reserved. No part of this document may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of Global Evolution, as applicable.

Copyright © 2026 Global Evolution - All rights reserved