Dear visitor

You tried to access but this page is only available for

You tried to access but this page is only available for

Witold Bahrke

Senior Macro and Allocation Strategist

Tactically, the Middle East escalation calls for a cautious stance on EMD risk exposure and core duration, in line with our recent top-down stance. Judged by the objectives and the amount of military resources deployed by the US as well as Iran regime’s willingness to retaliate amid its fight for survival, the conflict could be more long-lasting than the initial market reaction indicates. That said, the Washington’s aversion to higher oil prices and Iran’s limited military capabilities should prevent the conflict extending into the strategic investment horizon. In the same vein, sustained spikes in oil prices seems unlikely. While the range of outcomes has widened, this should not be a game-changer, neither for markets nor the business cycle.

“Epic Fury”: Worst escalation in decades

US and Israel have launched the most severe attack against Iran in decades. In the grand scheme of things, operation “epic fury” hardly came as a surprise (see chart 1) and showcases one of the most prominent top-down regime shifts we have highlighted for some time, namely the transitions from low towards higher geopolitical uncertainty.

However, it seems the consensus expected a more limited military operation, at least initially. The US’ apparent objective of achieving a regime change in Iran has not been aired beforehand. Teheran’s response has been more wide-ranging than anticipated. While many observers saw a military intervention coming, few analysts did expect Iranian attacks on civil targets in other gulf states and a de-facto closure of the Hormuz Strait, through which 20% of the world’s oil shipments are flowing.

Already at the current juncture it is therefore fair to say that the Middle East conflict has entered a new dimension. In order to assess the wider impact on the global economy as well as markets, the key question is how long the conflict will last.

Timeline: Not days, not months but probably weeks

There’s a lot to win but also a lot to lose for the involved parties, both economically and from a security perspective. Taking into account what appears to be the main parties core objectives, the military action is unlikely to last months. A resolution within days appears equally unlikely.

The US military build-up in the region is testament to the US wide-reaching ambitions, or as Trump put it, the US will do “whatever it takes” to achieve its objectives. Based on recent military actions and statements from the White House and Israel’s government, US and Israel prime objectives are to prevent Iran from becoming a nuclear power, destroy vast parts of its military resources and toppling the current regime.

For Washington, the oil price is also part of the equation. Here, the silver lining is that the US president wants to avoid higher oil prices into the mid-term elections. While this implicit objective should prevent the conflict from stretching over months, it also increases the incentive not to end the military campaign too soon as quick wins are a distant prospect in the region. Iran could ramp up it’s production much faster than e.g. Venezuela. To that end, the White House administration might see the current conflict as a once in a generation opportunity to achieve these goals. Based on our best judgement, it takes a serious reshuffling of the Iranian regime to pave the ground for a sustained increase in oil supplies and minimizing the risk of renewed disruptions in the future.

In other words, some kind of regime change or at a minimum a leadership reshuffling in Teheran is a necessary condition for achieving both security and economic objectives. The country’s leadership structure is very complex and the term “regime shift” can take many forms. While it takes the finishing line less clear than in previous military operations, it seems quite clear this objective will not be achieved within days, pointing towards an extended military campaign.

What about Iran? Given US and Israel’s goals described above, the Iranian regime - or at least the remaining parts of it - is fighting for its survival. As things stand, it has no obvious off-ramps. This makes Iran a less rational player. Consequently, it stated having “no red lines” when it comes to retaliatory responses. Granted, its military capabilities are severely hampered. Still, Iran should be able to e.g. impair oil flows from the region significantly for an extended time period. At the time of writing, Iran has claimed to close the Strait of Hormuz according to state media. Even before this headline broke, insurance companies withdrew their war-risk coverage which effectively causes oil flows through the strait to dry up.

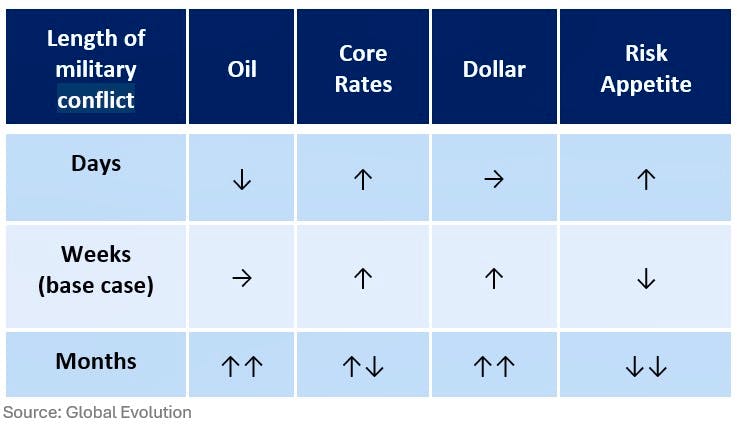

Altogether, the conflict looks to span over several weeks. However, uncertainty has jumped higher, as well. The combination of a very ambitious plan on the US/Israeli side and a desperate Iranian regime that feels it has its back to the wall implies a wide range of outcomes and fatter tail risks around the main scenario.

Although Teheran has refused to negotiate since the US and Israel started their attacks, one cannot rule out that the Iranian regime changes its mind in the elevenths hour and seeks to negotiate, causing the conflict to be halted within days. On the other hand, Iran remains something of a black box and we might underestimate the regime’s ability to cling to power and keep the conflict going. In that case, the conflict could take months and recession risks would re-emerge as oil prices take quantum leap higher, leading to a sharp sell-off in risk assets (see table 1).

Fundamentals: No game changer

It goes without saying that the key transmission mechanism between geopolitical risks in the Middle East and the economy at large is the oil price. On a positive note, the oil market finds itself in an ample supply regime and OPEC has already pledged to increase its daily oil supply by more than 200,000 barrels/day in response to the escalation. However, our suspicion is that markets are pricing a quick resolution, underestimating the risks of a prolonged conflict and Iran’s willingness to hit the wider oil infrastructure and trade channels. Therefore, we think current oil prices will prevail around current levels and could briefly spike significantly higher, although such moves should prove to be short-lived.

This adds to the near-term upside risk to inflation we highlighted in our recent outlook. The military conflict shouldn’t alter the trajectory of the overall business cycle, though, provided the conflict does not last several months and medium-term oil prices do mean-revert back to current levels. Military escalations of limited time spans tend not to have significant and long-lasting effects on overall growth. Even with oil prices remaining relatively high in the short-term, levels are far from extreme in a historic context, limiting the potential fallout from weaker household demand.

That said, differentiation is key. Oil importers will be hurt, while oil exporters could benefit from current developments. China, in particular, could be negatively impacted by higher oil prices over the coming months and a potential regime shift in Iran. It is an oil importer and has bought the bulk of Iranian oil. On the other hand, oil exporters outside the Middle East are among the winners relatively speaking, as they stand to benefit from higher oil prices while at the same time being shielded somewhat against a regional geopolitically-driven risk premium.

Markets: We’re not there, yet

Historically, such geopolitical events had “buy-the-dip” written all over them, presenting buying opportunities across a broad spectrum of risk assets. Ultimately, this time might not be all that different, offering attractive entry points further down the road. It is still early days but investors are seemingly taking comfort from historic precedence.

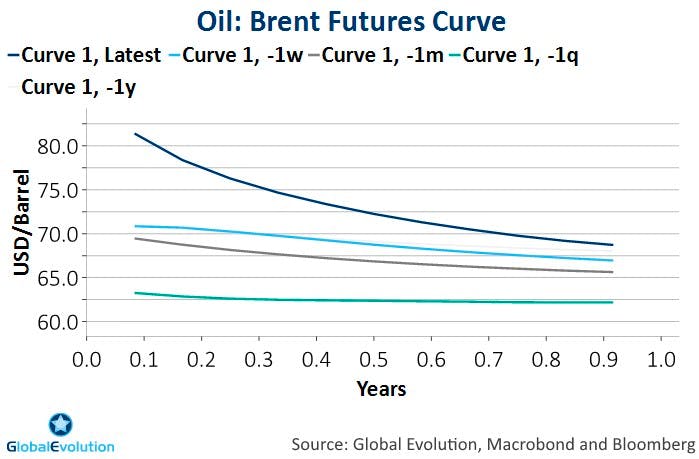

On the flipside, operation “epic fury” triggered fatter tail risks. Markets might underestimate the stamina of the major conflict parties US, Israel and Iran. The risk of a more prolonged period of geopolitical tensions, risk aversion and higher for longer oil prices (see chart 2) seems underpriced as oil futures downward trajectory has remained largely unchanged over the past months. Core rates and Fed’s expected rate path has moved higher in the first trading session after the attacks on Iran were launched, albeit moderately so. EM sovereign spreads barely reacted.

We are constructive when it comes to full year EM debt returns as the global economy remains resilient and fundamental datapoints (inflation, growth) support the case for EM debt (see the latest Global Evolution outlook here). We therefore believe tactical set-backs presents attractive entry points in e.g. lower-rated EM credit segments.

All being said, we’re not there yet as neither the US, Israel nor Iran has clear incentive to de-escalate within days. The trifecta of investors underpricing the risk of an extended conflict, stretched tactical indicators (sentiment, positioning and valuation) and additional inflation risks reinforces our tactically cautious stance on overall EMD risk exposure as well as core duration. Near-term, our base case therefore suggests higher oil prices, upside risks to core rates as inflation risks linger, downside risks to EM currencies and a bias towards further EM credit spread widening.

Positioning: Keeping some powder dry

Overall, our core strategies are well positioned for a period of higher oil prices, elevated market volatility, spread widening and EM FX depreciation risks. From a top-down perspective, we entered the year with a cautious tactical stance on overall EMD risk and duration. In an asset allocation context, our tactical preference for hard currency EM debt and USD strengthening should pay off. We have reduced the riskiest credit segments in the hard currency universe, bringing down overall portfolio betas. Although a resilient global economy should create attractive entry points in the longer-term, we are opting to keep some powder dry amid near-term spread-widening risk.

From a regional perspective, we have reduced the exposure to the Middel East and are now underweight the region in our hard currency sovereign strategy. On the local currency side, we have reduced positions in Romania and Hungary as Eastern Europe is the most vulnerable region when it comes to higher energy prices and Dollar strength. Additionally, we have trimmed exposure to South Africa, reflecting its high-beta characteristics and sensitivity to a risk-off USD environment. China, which is most exposed to higher oil prices in the near-term and disruption in Iranian oil supply, has been a significant underweight for some time. Meanwhile, our preference for Latin America should benefit from the Middle East conflict and higher oil prices as the region has many oil exporters, while at the same time being somewhat distanced from rising geopolitical risks in the Middle East region.

Turning to Frontier Markets, history has shown that this segment has weathered major EM and global drawdown periods relatively well. Furthermore, Frontier Markets debt has typically rebounded quickly from drawdowns, largely due to strong local investor participation, which reduces forced selling during global risk-off episodes. At the same time, the high carry component has supported overall returns.

As the Frontier strategy maintains a relatively low duration, it is less sensitive to global rate movements compared to comparable fixed income strategies. Currently, the Frontier blended strategy holds positions in 37 countries, of which only a handful are directly impacted by the escalation of the conflict.

Disclaimer & Important Disclosures

Global Evolution Asset Management A/S (“GEAM”) is incorporated in Denmark and authorized and regulated by the Danish FSA (Finanstilsynet). GEAM DK is located at Buen 11, 2nd Floor, Kolding 6000, Denmark.

GEAM has a United Kingdom branch (“Global Evolution Asset Management A/S (London Branch)”) located at Level 8, 24 Monument Street, London, EC3R 8AJ, United Kingdom. This branch is authorized and regulated by the Financial Conduct Authority under FCA # 954331. In Canada, while GEAM has no physical place of business, it has filed to claim the international dealer exemption and international adviser exemption in Alberta, British Columbia, Ontario, Quebec and Saskatchewan.

In the United States, investment advisory services are offered through Global Evolution USA, LLC (‘Global Evolution USA”), a Securities and Exchange Commission (“SEC”) registered investment advisor. Global Evolution USA is located at: 250 Park Avenue, 15th floor, New York, NY. Global Evolution USA is a wholly owned subsidiary of Global Evolution Financial ApS, the holding company of GEAM. Portfolio management and investment advisory services are provided to GE USA clients by GEAM. GEAM is exempt from SEC registration as a “participating affiliate” of Global Evolution USA as that term is used in relief granted by the staff of the SEC allowing U.S. registered investment advisers to use investment advisory resources of non-U.S. investment adviser affiliates subject to the regulatory supervision of the U.S. registered investment adviser. Registration with the SEC does not imply any level of skill or expertise. Prior to making any investment, an investor should read all disclosure and other documents associated with such investment including Global Evolution’s Form ADV which can be found at https://adviserinfo.sec.gov.

In Singapore, Global Evolution Fund Management Singapore Pte. Ltd (“Global Evolution Singapore”) has a Capital Markets Services license issued by the Monetary Authority of Singapore for fund management activities. It is located at Level 39, Marina Bay Financial Centre Tower 2, 10 Marina Boulevard, Singapore 018983.

GEAM, Global Evolution USA, and Global Evolution Singapore, together with their holding companies, Global Evolution Financial Aps and Global Evolution Holding Aps, make up the Global Evolution group affiliates (“Global Evolution”).

Global Evolution, Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC, and Pearlmark Real Estate, L.L.C. and its subsidiaries are all direct or indirect subsidiaries of Conning Holdings Limited (collectively, “Conning”) which is one of the family of companies whose controlling shareholder is Generali Investments Holding S.p.A. (“GIH”) a company headquartered in Italy. Assicurazioni Generali S.p.A. is the ultimate controlling parent of all GIH subsidiaries. Conning has investment centers in Asia, Europe and North America.

Conning, Inc., Conning Investment Products, Inc., Goodwin Capital Advisers, Inc., Octagon Credit Investors, LLC, PREP Investment Advisers, L.L.C. and Global Evolution USA, LLC are registered with the SEC under the Investment Advisers Act of 1940 and have noticed other jurisdictions they are conducting securities advisory business when required by law. In any other jurisdictions where they have not provided notice and are not exempt or excluded from those laws, they cannot transact business as an investment adviser and may not be able to respond to individual inquiries if the response could potentially lead to a transaction in securities.

Conning, Inc. is also registered with the National Futures Association. Conning Investment Products, Inc. is also registered with the Ontario Securities Commission. Conning Asset Management Limited is Authorised and regulated by the United Kingdom's Financial Conduct Authority (FCA#189316); Conning Asia Pacific Limited is regulated by Hong Kong’s Securities and Futures Commission for Types 1, 4 and 9 regulated activities; Global Evolution Asset Management A/S is regulated by Finanstilsynet (the Danish FSA) (FSA #8193); Global Evolution Asset Management A/S (London Branch) is regulated by the United Kingdom's Financial Conduct Authority (FCA# 954331); Global Evolution Asset Management A/S, Luxembourg branch, registered with the Luxembourg Company Register as the Luxembourg branch(es) of Global Evolution Asset Management A/S under the reference B287058. It is also registered with the CSSF under the license number S00009438. Conning primarily provides asset management services for third-party assets.

This publication is for informational purposes and is not intended as an offer to purchase any security. Nothing contained in this communication constitutes or forms part of any offer to sell or buy an investment, or any solicitation of such an offer in any jurisdiction in which such offer or solicitation would be unlawful.

All investments entail risk, and you could lose all or a substantial amount of your investment. Past performance is not indicative of future results which may differ materially from past performance. The strategies presented herein invest in foreign securities which involve volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging and frontier markets. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, and credit.

The Agent of Capital Strategies Partners in respect of the placement of Global Evolution Frontier Markets in the United States is Marco Polo Securities Inc, a non-affiliated broker-dealer registered with the US Securities and Exchange Commission. The activities of Capital Strategies Partners in the United States, including the distribution of Indicative Term Sheets, will be effected only to the extent permitted by Rule 15a-6 under the US Securities Exchange Act of 1934 and in accordance with the Services Agreement entered into between Capital Strategies Partners and Marco Polo Securities Inc with respect thereto. Marco Polo Securities Inc. is a FINRA registered broker-dealer (CRD# 46561) formed for that purpose in the State of New York with its principal office at 1230 Avenue of the Americas, 16th floor, New York, New York, 10020. Contact at Marco Polo Securities is clientservices@mpsecurities.com ; 1-347-745-6448.

While reasonable care has been taken to ensure that the information herein is factually correct, Global Evolution makes no representation or guarantee as to its accuracy or completeness. The information herein is subject to change without notice. Certain information contained herein has been provided by third party sources which are believed to be reliable, but accuracy and completeness cannot be guaranteed. Global Evolution does not guarantee the accuracy of information obtained from third party/other sources.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

Legal Disclaimer ©2026 Global Evolution.

This document is copyrighted with all rights reserved. No part of this document may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of Global Evolution, as applicable.

Copyright © 2026 Global Evolution - All rights reserved