Dear visitor

You tried to access but this page is only available for

You tried to access but this page is only available for

Michael Wainø Hansen

Senior Strategist

Trump is Back in Full Force

Donald Trump has not wasted any time since his inauguration on January 20 as the 47th President of the United States. If the world was already breathless over his many tweets in the weeks following the presidential election on November 5, 2024, the global order and traditional conventions—including international law—are now under attack from the American administration’s unconventional policies in almost every area, including taxation, healthcare, the environment, foreign trade, aid, and international diplomacy. Traditional U.S. allies are openly threatened with economic sanctions if they do not comply, and in some cases, President Trump has refused to rule out the possibility of using military force to secure his administration’s definition of American interests.

Regarding the latter, Denmark and Panama have been targeted due to President Trump's plans for an American annexation of Greenland and the Panama Canal. Canada has also been a target of Trump’s territorial ambitions, as he proposed that Canada could become the 51st U.S. state, arguing that Canada owes the U.S. a significant amount of money and that the U.S. already subsidizes and provides military protection for Canada. However, on February 5, the world was left completely stunned when Trump, during a press conference with Israeli Prime Minister Netanyahu, suggested that the U.S. could take over the Gaza Strip, deport the Palestinians to Jordan and Egypt, and create the "Riviera of the Middle East." In this respect, Jordan and Egypt felt the heat, as Trump floated the idea that the two countries should take in 2million Palestinians from the Gaza Strip.

While it may be difficult to understand Trump’s rationale for directly involving the U.S. in a historically religious and cultural powder keg like Gaza, the reasoning behind taking control of the Panama Canal and Greenland is more straightforward—it’s about geopolitics, minerals and shipping routes. Still, implied threats of annexation through military force are in direct conflict with the principles of international law regarding territorial sovereignty. According to these principles, states are only competent to exercise their power—legislative, judicial, and especially in the form of police and military force—within their own territory, unless they act in self-defense.

The U.S. Has a History of Land Purchases

Donald Trump seems to show limited regard for international law, and while the idea of an American purchase of Greenland supported by military threats may appear unrealistic, absurd, or unusual in Denmark and other parts of Western Europe, buying land and annexation have often been part of American history.

For example, between 1803 and 1898, the U.S. tripled its geographical size through the purchase of Louisiana (from France), Florida (from Mexico), and Alaska (from Russia), as well as the annexation of Texas (which had declared independence from Mexico), which subsequently led to the Mexican-American War over the demarcation between Texas and Mexico. Later, in 1927, the Virgin Islands were purchased from Denmark.

When President Trump does not rule out the use of force in relation to Greenland, it can be seen as a direct continuation of the so-called Monroe Doctrine from 1823. This doctrine was named after President James Monroe, who, in his annual address to Congress, warned European nations that the U.S. would not tolerate further colonization or the installation of puppet governments in countries within the American sphere of interest. In 1865, the Monroe Doctrine was put into practice when the U.S. government used diplomacy and military pressure to support Mexican President Juárez in a successful revolt against Emperor Maximilian, who had been placed on the throne with French assistance.

Later, in 1904, when European creditor nations threatened Latin American countries with military intervention to collect debts, President Roosevelt proclaimed the U.S. right to conduct “international police work” to prevent “chronic wrongdoing.” U.S. Marines also occupied Santo Domingo in 1904, Nicaragua in 1911, and Haiti in 1915, primarily to keep European nations out. In 1962, when the Soviet Union began constructing missile launch sites in Cuba, President Kennedy implemented a naval blockade of Cuba, symbolically invoking the Monroe Doctrine[1].

Why Trump Wants Greenland

Geographically, Greenland holds strategic importance for the United States. This is nothing new, which is why the U.S. has maintained a military presence at the Pituffik Space Base (formerly Thule Air Base) for many years. Today, the base is a critical part of the U.S. early missile warning system. However, over the past 5–10 years, increasing geopolitical tensions between the U.S. and Western Europe on one side and Russia and China on the other have brought renewed focus on Greenland—not only as a bastion for military defense systems but also as a key player in the battle for sovereignty over and control of new maritime trade routes opening up as Arctic ice continues to melt (more on this later).

Additionally, Greenland's underground is rich in rare minerals, which are crucial for the green transition but are primarily found in countries like China and Russia. This makes rare minerals potential tools in trade and geopolitical power struggles as seen in early February 2025, when China restricted its export to the U.S. of tungsten, tellurium, bismuth, molybdenum and indium on top of a ban on exports of gallium, geranium and antimony announced in December 2024. China’s vast resources of rare minerals are hard to substitute and those other nations with significant mining and reserves of rare minerals cannot always be considered the West’s closest allies, but overall, going forward we believe that Western countries increasingly will prioritize sourcing rare minerals from emerging market countries be it in Latin America, Africa, and Asia (excluding China) over supplies from China and Russia.

Ukraine is the latest country to experience U.S. bargaining tactics and its strategic interest in controlling rare minerals. The Trump administration has proposed that the United States receive access to 50% of Ukraine’s rare earth minerals—valued at $500 billion—in exchange for U.S.-backed security measures following a ceasefire and the eventual resolution of the war with Russia.

In a February 7, 2025, interview with Reuters, Ukrainian President Volodymyr Zelenskiy indicated openness to such an agreement while emphasizing that less than 20% of Ukraine’s mineral resources are currently under Russian control. According to Ukrainian data, the country holds deposits of 22 out of the 34 minerals classified as critical by the European Union[2].

Greenland’s estimated reserves of rare metals stand at 1.5 million tons, nearly matching the known reserves in the U.S. These reserves include 43 of the 50 minerals deemed critical by the U.S. government. In addition to rare metals, Greenland also holds reserves of oil, gas, and freshwater. However, there is currently no active mining operation in Greenland.

Greenland Heads to the Polls

Both Denmark and Greenland have made it clear that Greenland is not for sale. From the Danish side, the message is that Greenland’s future is largely up to the Greenlandic people, while Greenlandic politicians emphasize that Greenland belongs to the Greenlanders though they remain open to cooperation with the United States. The question is whether Trump will be satisfied with cooperation on Greenland’s terms.

Greenland’s Premier Egede recently called for a national election to be held on March 11, 2025. This will be the first time Egede runs for re-election as the sitting premier after he and his party, Inuit Ataqatigiit (IA), won the 2021 election on a platform that included banning the extraction of rare minerals and uranium in a large-scale mining project at Kvanefjeld near Narsaq. If Premier Egede and Inuit Ataqatigiit (IA) now to appease Donald Trump decide to open up for mining co-operation, it would mark a significant policy reversal.

The Polar Silk Road

Climate change and the retreat of the Arctic ice cap are other key factors driving not only U.S. interest in Greenland but also Russia’s and China’s broader ambitions in the Arctic region.

According to UNESCO World Heritage, Greenland’s glaciers rank among those with the second and fifth largest ice loss worldwide between 2000 and 2020. Ilulissat Icefjord recorded a loss of 350 billion tons, while Aasivissuit Nipisat lost 39 billion tons. Ilulissat Icefjord is second only to Kluane/Wrangell-St. Elias/Glacier Bay in Alaska, which saw a reduction of 487 billion tons.

A study by the Universities of Edinburgh and Zurich shows that the world’s glaciers from 2000 to 2023 collective lost 6.542 trillion tons of ice or 273bn tons per year. According to the study, the former number has raised global sea levels by 1.8cm while the latter number is equivalent to 30years of water consumption by the entire global population.

Ocean shipping is the backbone of global trade and an integral part of industrial supply chains. With globalization accelerating in the 2000s, the volume of goods transported by sea has more than doubled from 1990 to the 2020s and today accounts for approximately 80% of total global goods transport.

As early as 2018, China recognized that climate change could open new maritime trade routes in the Arctic and launched the "Polar Silk Road" project, seeking closer ties with Iceland and Norway through commercial interaction and to this day, China maintains its "Yellow River" research station in Svalbard, Norway, which was established in 2003.

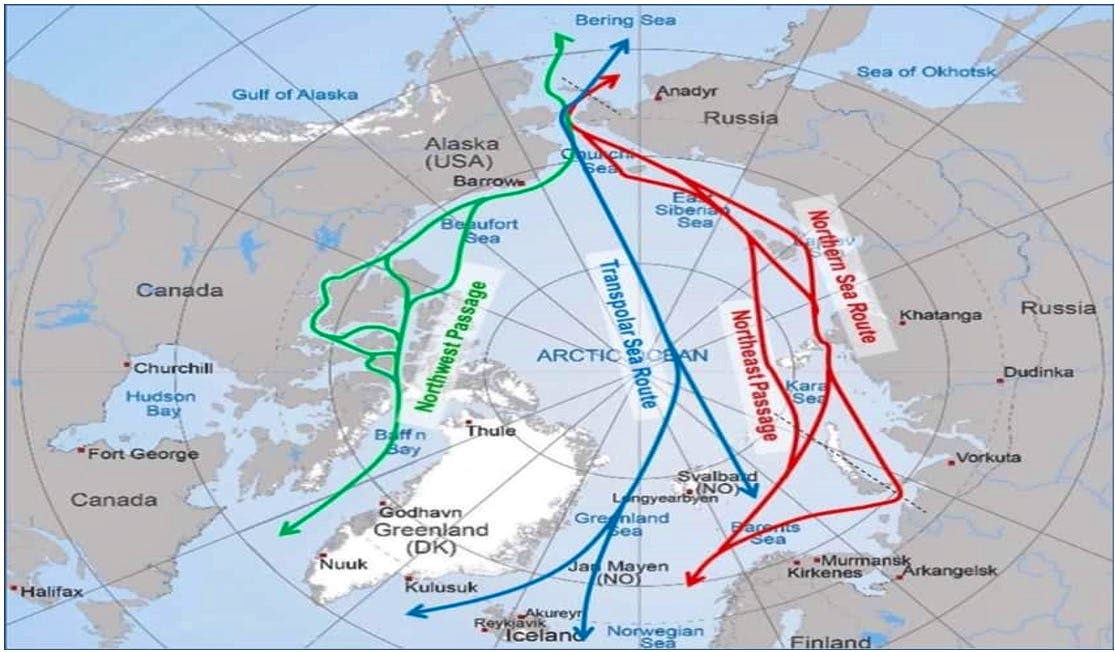

The Major Shipping Routes Expected to Become Navigable Are:

1. Northern Sea Route (NSR) – Along Russia’s Arctic Coast

This route is expected to be the first to become ice-free due to climate change. It will shorten the sea journey between East Asia and Western Europe from approximately 21,000 km via the Suez Canal to about 12,800 km, reducing travel time by 10–15 days. As early as 2018, the Danish-owned ice-class container ship Venta Maersk successfully completed a trial voyage along the NSR, carrying 3,600 containers. In 2024, the 295-meter-long Panamax container ship Flying Fish 1 became the first vessel of its class to complete the route without an icebreaker escort.

2. Northwest Passage (NWP) – Along Canada’s Arctic Coast/Islands

Historically, this passage has been blocked by ice, but ice coverage is now rapidly declining. In 2024, for the first time in recorded meteorological history, the route was open during the summer months. The passage will shorten the sea journey between East Asia and Western Europe by approximately 13,600 km.

3. Transpolar Route (TPR) – Directly Across the Arctic Ocean

This route would require complete melting of Arctic ice, which is unlikely to happen in the coming many decades.

4. The Arctic Bridge

Though not strictly an Arctic Sea route, this corridor connects Murmansk, Russia, and Narvik, Norway, with the Canadian port city of Churchill. In the future, it could be used for transporting commodities such as grain.

The new Arctic shipping routes are not only of commercial interest due to shorter transit times and lower transportation costs (fuel and canal fees) but also play a crucial role in supply chain security and geopolitical risk mitigation. For example, in 2021, the Suez Canal was blocked for six days when a grounded vessel obstructed passage causing significant logistical disruptions worldwide. For shipping company Maersk the result of this was a loss of nearly USD 89mn.

Furthermore, since the outbreak of the Israel-Hamas war in 2023, Houthi militants have attacked more than 100 ships in the Red Sea and the Gulf of Aden, forcing shipping companies to reroute vessels via the much longer route around the Cape of Good Hope in South Africa.

Winners and losers

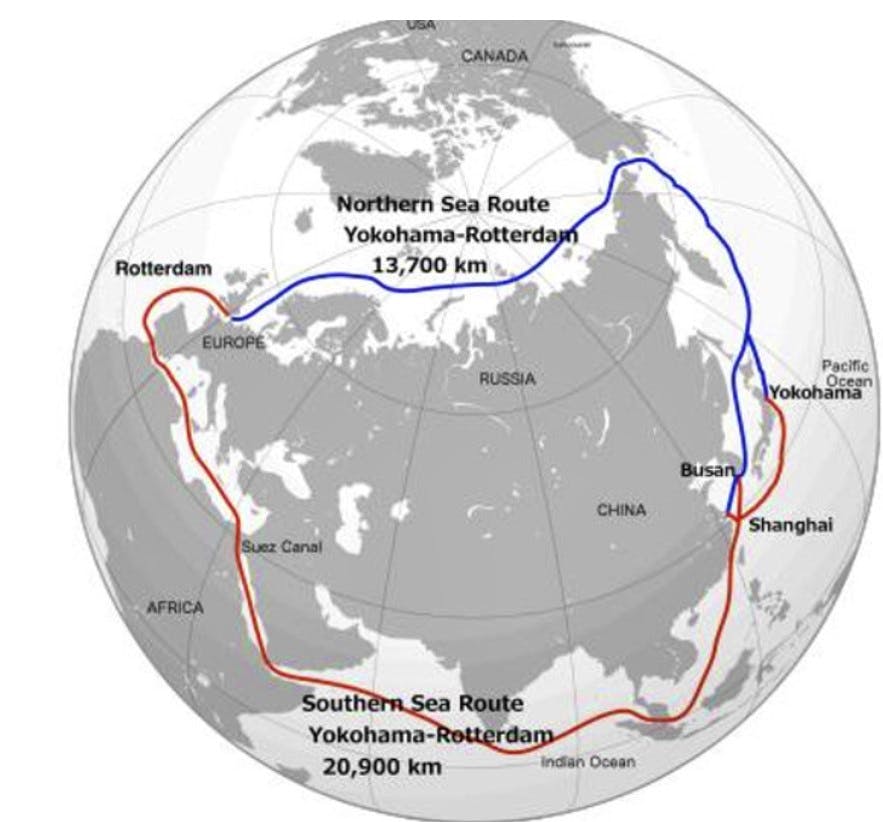

While the shorter Arctic shipping routes could, in a best-case scenario, enhance global trade, reduce inflation worldwide, and boost infrastructure projects in the countries along these routes, the outlook is far less positive for Egypt and Panama. For them, the Arctic routes would directly compete with the Suez Canal and the Panama Canal.

In 2023, Egypt generated USD 10.2 billion in canal revenues from 26,400 vessels passing through the Suez Canal. However, revenues dropped to USD 4 billion in 2024 due to ongoing geopolitical tensions in the Red Sea, which forced shipping companies to reroute their vessels. Ship traffic also declined to 13,200 vessels. The Egyptian canal authorities expect revenues to recover to USD 9 billion in 2025, but in the long run, the loss of canal revenue could be substantial, depending on how many shipping companies choose the Arctic Silk Road over the Suez Canal.

Panama, meanwhile, recorded USD 4.5 billion in canal revenues in 2023 from approximately 14,000 vessels. The route from Shanghai to New York via the Arctic Silk Road is 30–40% shorter than the route through the Panama Canal, providing a significant economic incentive for shipping companies to switch routes.

The future commercial viability of Arctic shipping routes remains uncertain. While these routes offer shorter distances, this does not necessarily result in proportionally reduced transit times or cost savings. Several factors influence feasibility, including fuel and insurance costs, load factors, unit transportation expenses, wages, tolls (such as those for the Suez Canal and the Northern Sea Route), and port stops.

Arctic sea ice coverage fluctuates yearly but has shown a consistent decline over decades. According to NASA and NSIDC, the Arctic has lost approximately 77,800 km² of sea ice annually since the late 1970s. Beyond shrinking in extent, the ice is also becoming thinner, with most of today’s Arctic ice being first-year ice, which is more prone to melting during warmer months.

If this trend continues, Arctic shipping routes may become more viable and profitable. Countries along these emerging routes could see increased infrastructure investments, while those along the traditional shipping corridor—linking China, Korea, and Japan to Europe via the Strait of Malacca and the Suez Canal—may experience reduced investments and declining revenues from ports and service hubs.

Emissions and the Arctic Ecosystem

Finally, there is the issue of CO2 emissions, the environment, and the Arctic ecosystem. While shorter shipping routes and reduced fuel consumption should lower CO2 emissions, increased maritime traffic and the potential for oil spills in these waters could pose a serious threat to the entire ecosystem.

The Militarization of the Arctic

In 1946, the U.S. Joint Chiefs of Staff determined that Greenland and Iceland were essential international locations for American military bases. That same year, U.S. Secretary of State James Byrnes offered to purchase Greenland from Denmark for USD 100 million.

In more recent times, the U.S. Department of Defense, in its 2024 Arctic Strategy, warned that Russia’s maritime infrastructure could lead to “excessive and illegal maritime claims” along the NSR shipping route. Additionally, cooperation between Russia and China in the region is seen as a cause for concern. As recently as December 2024, China successfully launched a maiden voyage with a "polar-ready" 58,000-ton cargo ship and has referred to itself as a “near-Arctic state” to legitimize its interest in the region.

Russia’s Northern Fleet has significantly increased both surface and underwater monitoring in recent years, and—following upgrades to Soviet-era facilities—now has a larger military presence in the Arctic than NATO. However, NATO has also bolstered its presence through military exercises and organic expansion, particularly with the recent accession of Sweden and Finland into the alliance.

In 2024, the U.S., Canada, and Finland formalized a cooperative agreement known as the ICE PACT, aimed at securing and maintaining their influence in the Arctic region. To achieve this, the three countries plan to jointly build 90 icebreakers to counter Russian and Chinese ambitions in the Arctic. Canadian authorities have explicitly stated that the ICE PACT has military objectives intended to assert “Arctic sovereignty.”

By comparison, Russia currently operates a fleet of 57 icebreakers and Arctic-capable patrol vessels, while Canada has 18, Finland has 10, and the U.S. has only 5.

The map below illustrates the locations of arctic military bases controlled by Russia and NATO member states, including the U.S., Canada, Denmark, Finland, Norway, and Iceland.

The Future Awaits

The geopolitical power struggle is difficult to predict. One thing, however, is certain: the U.S., China and Russia see opportunities in the Arctic—whether due to the region's natural resources (oil, gas, and metals essential for the green transition), its potential shipping routes, or its military significance as an early missile warning zone.

It is still too early to say with certainty whether the alternative shipping routes through the Arctic will become a commercial success. However, if they do, these shorter trade routes could facilitate increased global trade, lower transportation costs, and, hopefully, reduce global inflation. While current U.S. trade policy has put globalization in reverse, looking beyond the next four years, all possibilities remain open.

Aside from the negative impact on Egypt’s and Panama’s canal revenues, we do not expect emerging markets as a whole to be negatively affected by the Arctic shipping routes or the geopolitical power struggle, including their positioning regarding green metals and rare earth elements. On the contrary, we expect that emerging markets could benefit from increased global trade and a Western shift away from dependence on China as the primary supplier of rare minerals.

Disclaimer & Important Disclosures

Global Evolution Asset Management A/S (“GEAM”) is incorporated in Denmark and authorized and regulated by the Finanstilsynets of Denmark (the “Danish FSA”). GEAM DK is located at Buen 11, 2nd Floor, Kolding 6000, Denmark.

GEAM has a United Kingdom branch (“Global Evolution Asset Management A/S (London Branch)”) located at Level 8, 24 Monument Street, London, EC3R 8AJ, United Kingdom. This branch is authorized and regulated by the Financial Conduct Authority under FCA # 954331. In Canada, while GEAM has no physical place of business, it has filed to claim the international dealer exemption and international adviser exemption in Alberta, British Columbia, Ontario, Quebec and Saskatchewan.

In the United States, investment advisory services are offered through Global Evolution USA, LLC (‘Global Evolution USA”), a Securities and Exchange Commission (“SEC”) registered investment advisor. Global Evolution USA is located at: 250 Park Avenue, 15th floor, New York, NY. Global Evolution USA is a wholly owned subsidiary of Global Evolution Financial ApS, the holding company of GEAM. Portfolio management and investment advisory services are provided to GE USA clients by GEAM. GEAM is exempt from SEC registration as a “participating affiliate” of Global Evolution USA as that term is used in relief granted by the staff of the SEC allowing U.S. registered investment advisers to use investment advisory resources of non-U.S. investment adviser affiliates subject to the regulatory supervision of the U.S. registered investment adviser. Registration with the SEC does not imply any level of skill or expertise. Prior to making any investment, an investor should read all disclosure and other documents associated with such investment including Global Evolution’s Form ADV which can be found at https://adviserinfo.sec.gov.

In Singapore, Global Evolution Fund Management Singapore Pte. Ltd (“Global Evolution Singapore”) has a Capital Markets Services license issued by the Monetary Authority of Singapore for fund management activities. It is located at Level 39, Marina Bay Financial Centre Tower 2, 10 Marina Boulevard, Singapore 018983.

GEAM, Global Evolution USA, and Global Evolution Singapore, together with their holding companies, Global Evolution Financial Aps and Global Evolution Holding Aps, make up the Global Evolution group affiliates (“Global Evolution”).

Global Evolution, Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC, and Pearlmark Real Estate, L.L.C. and its subsidiaries are all direct or indirect subsidiaries of Conning Holdings Limited (collectively, “Conning”) which is one of the family of companies whose controlling shareholder is Generali Investments Holding S.p.A. (“GIH”) a company headquartered in Italy. Assicurazioni Generali S.p.A. is the ultimate controlling parent of all GIH subsidiaries. Conning has investment centers in Asia, Europe and North America.

Conning, Inc., Conning Investment Products, Inc., Goodwin Capital Advisers, Inc., Octagon Credit Investors, LLC, PREP Investment Advisers, L.L.C. and Global Evolution USA, LLC are registered with the SEC under the Investment Advisers Act of 1940 and have noticed other jurisdictions they are conducting securities advisory business when required by law. In any other jurisdictions where they have not provided notice and are not exempt or excluded from those laws, they cannot transact business as an investment adviser and may not be able to respond to individual inquiries if the response could potentially lead to a transaction in securities.

Conning, Inc. is also registered with the National Futures Association. Conning Investment Products, Inc. is also registered with the Ontario Securities Commission. Conning Asset Management Limited is Authorised and regulated by the United Kingdom's Financial Conduct Authority (FCA#189316); Conning Asia Pacific Limited is regulated by Hong Kong’s Securities and Futures Commission for Types 1, 4 and 9 regulated activities; Global Evolution Asset Managment A/S is regulated by Finanstilsynet (the Danish FSA) (FSA #8193); Global Evolution Asset Management A/S (London Branch) is regulated by the United Kingdom's Financial Conduct Authority (FCA# 954331); Global Evolution Asset Management A/S, Luxembourg branch, registered with the Luxembourg Company Register as the Luxembourg branch(es) of Global Evolution Asset Management A/S under the reference B287058. It is also registered with the CSSF under the license number S00009438.. Conning primarily provides asset management services for third-party assets.

This publication is for informational purposes and is not intended as an offer to purchase any security. Nothing contained in this communication constitutes or forms part of any offer to sell or buy an investment, or any solicitation of such an offer in any jurisdiction in which such offer or solicitation would be unlawful.

All investments entail risk, and you could lose all or a substantial amount of your investment. Past performance is not indicative of future results which may differ materially from past performance. The strategies presented herein invest in foreign securities which involve volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging and frontier markets. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, and credit.

While reasonable care has been taken to ensure that the information herein is factually correct, Global Evolution makes no representation or guarantee as to its accuracy or completeness. The information herein is subject to change without notice. Certain information contained herein has been provided by third party sources which are believed to be reliable, but accuracy and completeness cannot be guaranteed. Global Evolution does not guarantee the accuracy of information obtained from third party/other sources.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

Legal Disclaimer ©2025 Global Evolution.

This document is copyrighted with all rights reserved. No part of this document may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of Global Evolution, as applicable.

Copyright © 2026 Global Evolution - All rights reserved