Dear visitor

You tried to access but this page is only available for

You tried to access but this page is only available for

Witold Bahrke

Senior Macro and Allocation Strategist

A short Q2 2026 outlook

MACRO: Teflon cycle shrugging off another supply shock

Growth: The business cycle is well-supported by past monetary easing, fiscal stimulus & an accelerating capex cycle. The 2W cease fire between the US and Iran should mark the beginning of a path towards deescalation. Oil is set to decline but remaining above the pre-war baseline, partly removing upside potential to global growth.

Inflation: Temporary inflation boost from energy but no 2nd round effects – provided oil settles below 100 USD/brl. Global inflation remains sticky above most central banks targets.

Policy: Fiscal stimulus remains a tailwind, monetary conditions tightening moderately.

Key risks: A full resolution to the Iran war & sanction removal triggering a positive supply shock & monetary easing. On the downside, a renewed closure of the Strait of Hormuz would cause a double whammy of high energy prices and monetary tightening leading to a recession.

MARKETS: Old habits die hard - buy into geopolitical stress & stagflation fears

Review: Our out-of-consensus expectation of a wobbly H1 (fading monetary tailwinds, stretched sentiment and geopolitical risks) is on track. We went into the Iran war defensively positioned & underweight local EMD.

Turning tactically bullish as geopolitical risks subside: Trump’s low approval ratings & spiking gasoline prices creates sufficient incentive for Washington to de-escalate over the coming weeks. Oil supply disruption should have peaked, accordingly. EM FX set to rebound – overweight local EMD in Q2 as positioning has cleared.

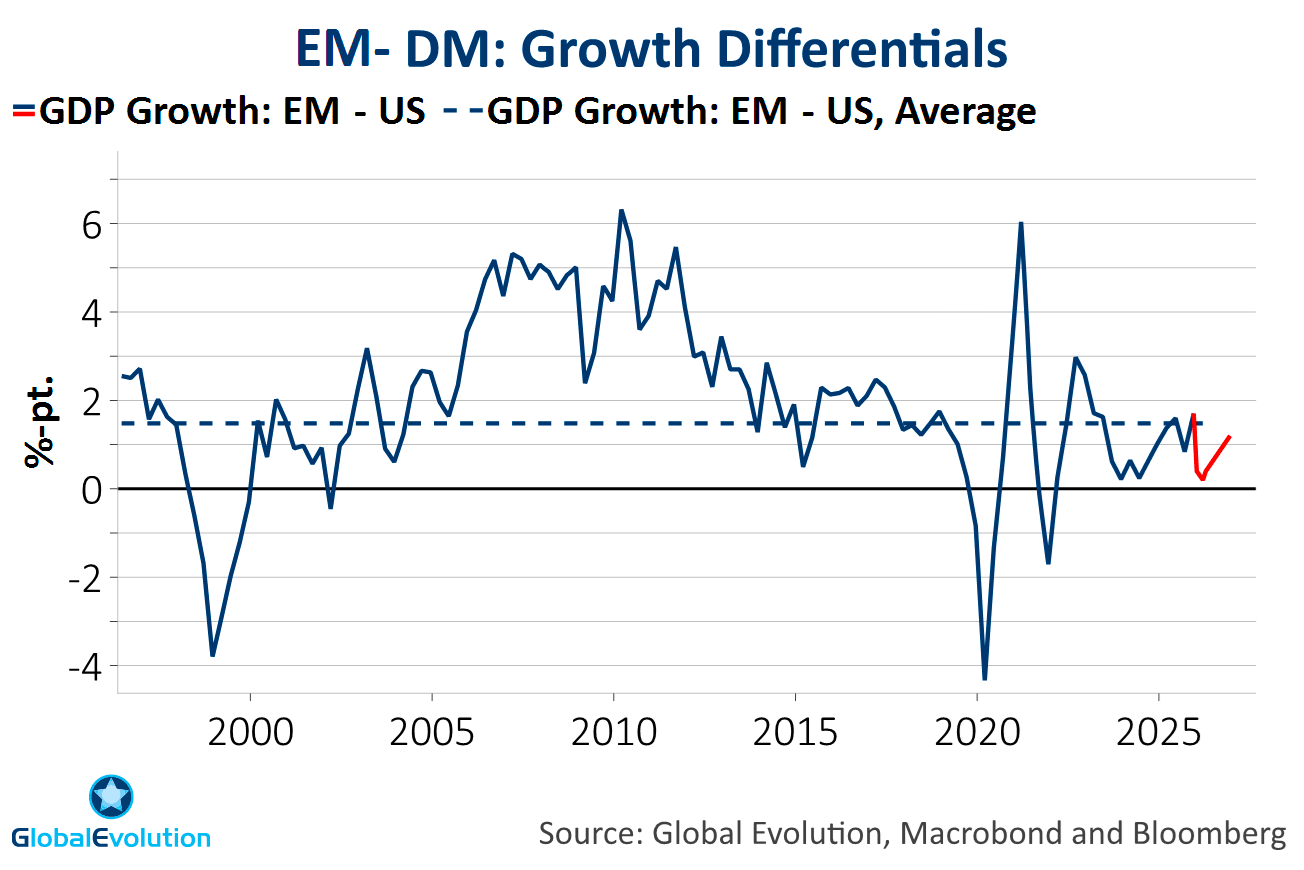

Strategic horizon: We expect high single-digit total returns driven by carry, but also capital gains as hiking expectations give way to limited cuts on a 12M horizon. Higher oil prices means the growth gap between the US and the RoW is moving more in US favour than expected 3M ago: O/W hard currency EMD (RHS chart). Monetary tightening creating a more unstable market equilibrium, arguing for a tactical approach to markets.

Supply shocks keep coming thick and fast (pandemic, Ukraine, tariffs, US immigration, Iran)…

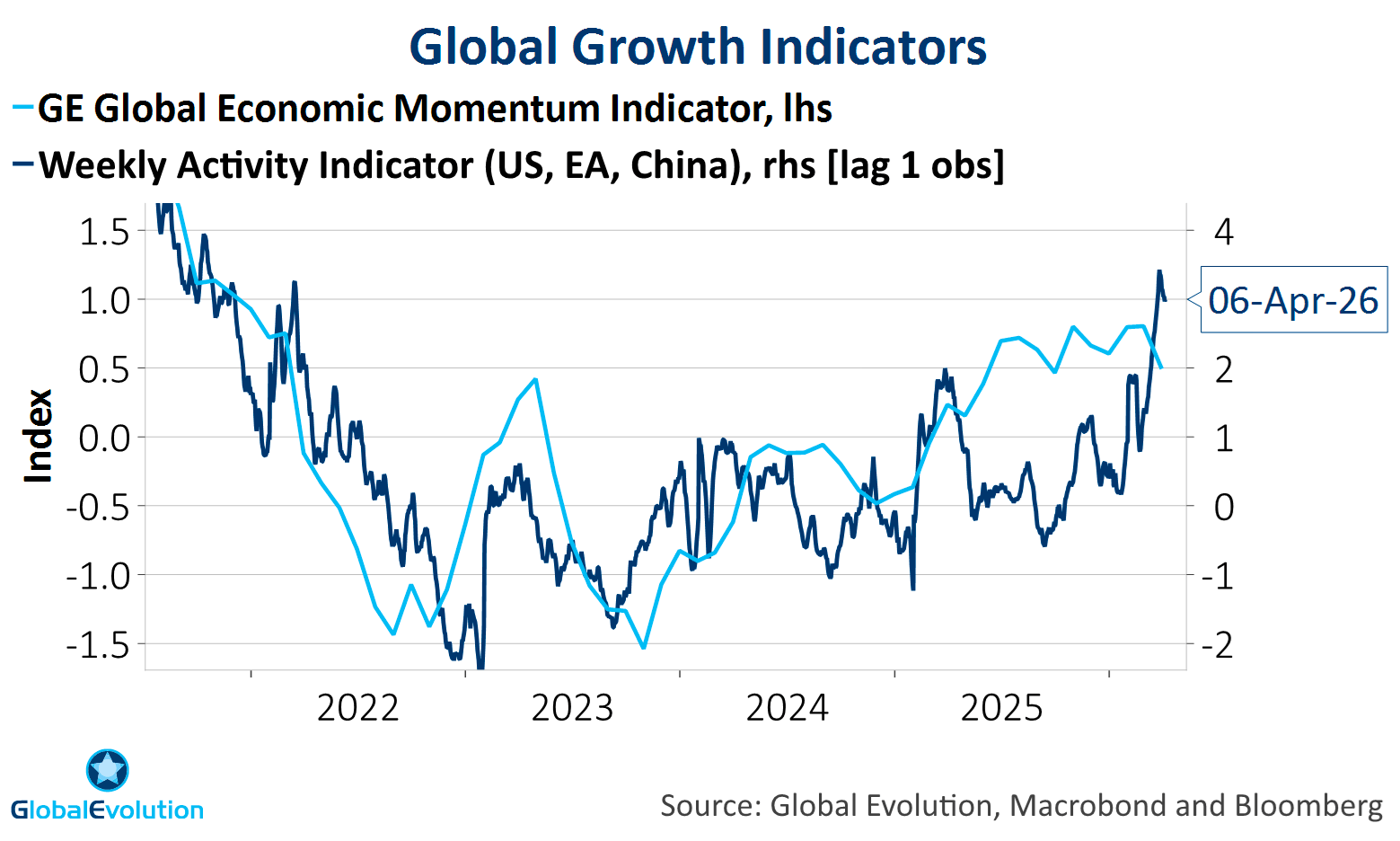

…but the business cycle isn’t budging: Even high-frequent indicators showing no signs of levelling off (LHS).

If our base case of a de-escalation in the Middle East proves to be correct, the capex cycle is supported by declining trade policy uncertainty (RHS).

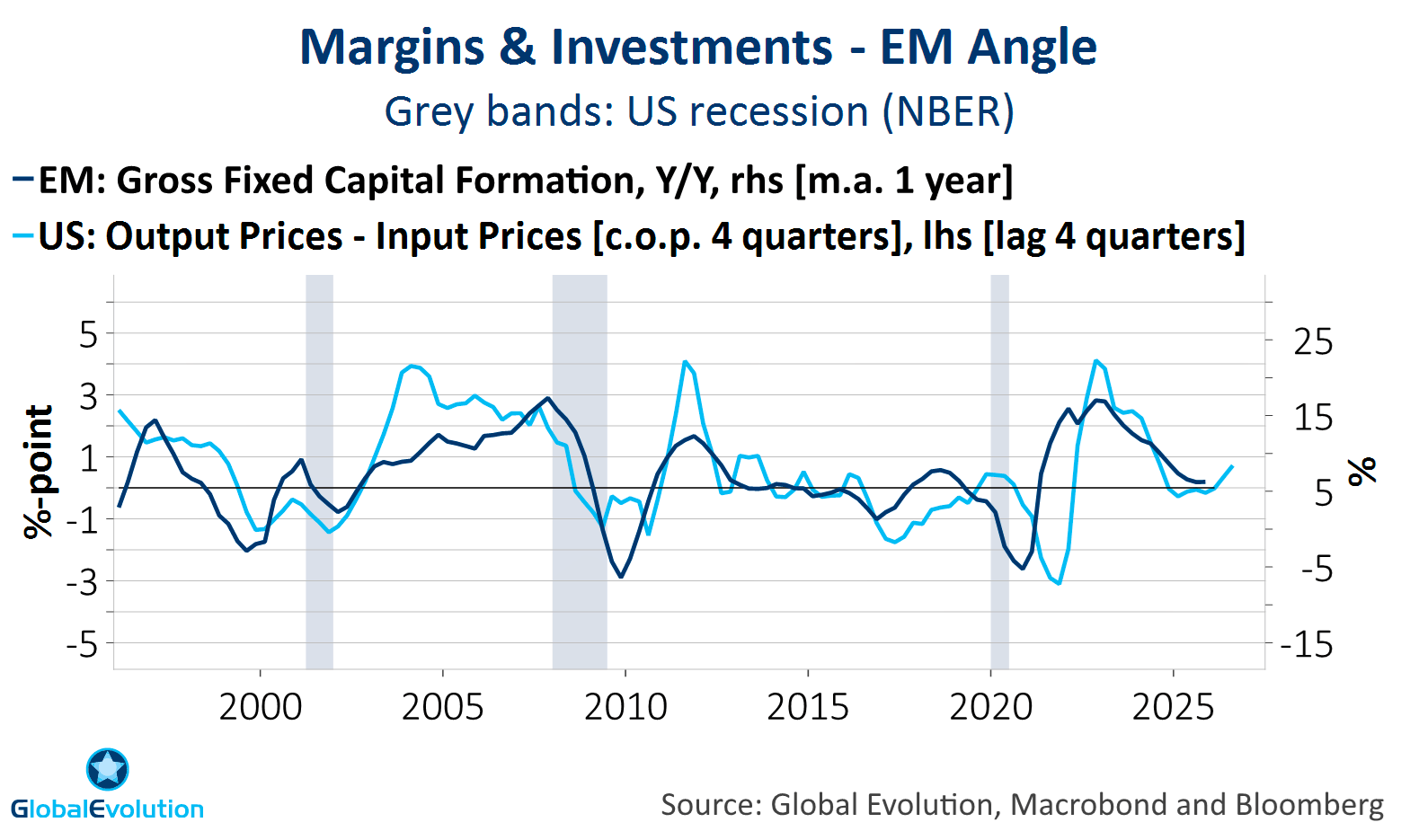

Cycle maturing, but remaining resilient: Besides capex, past monetary easing and expansive fiscal policy supports growth.

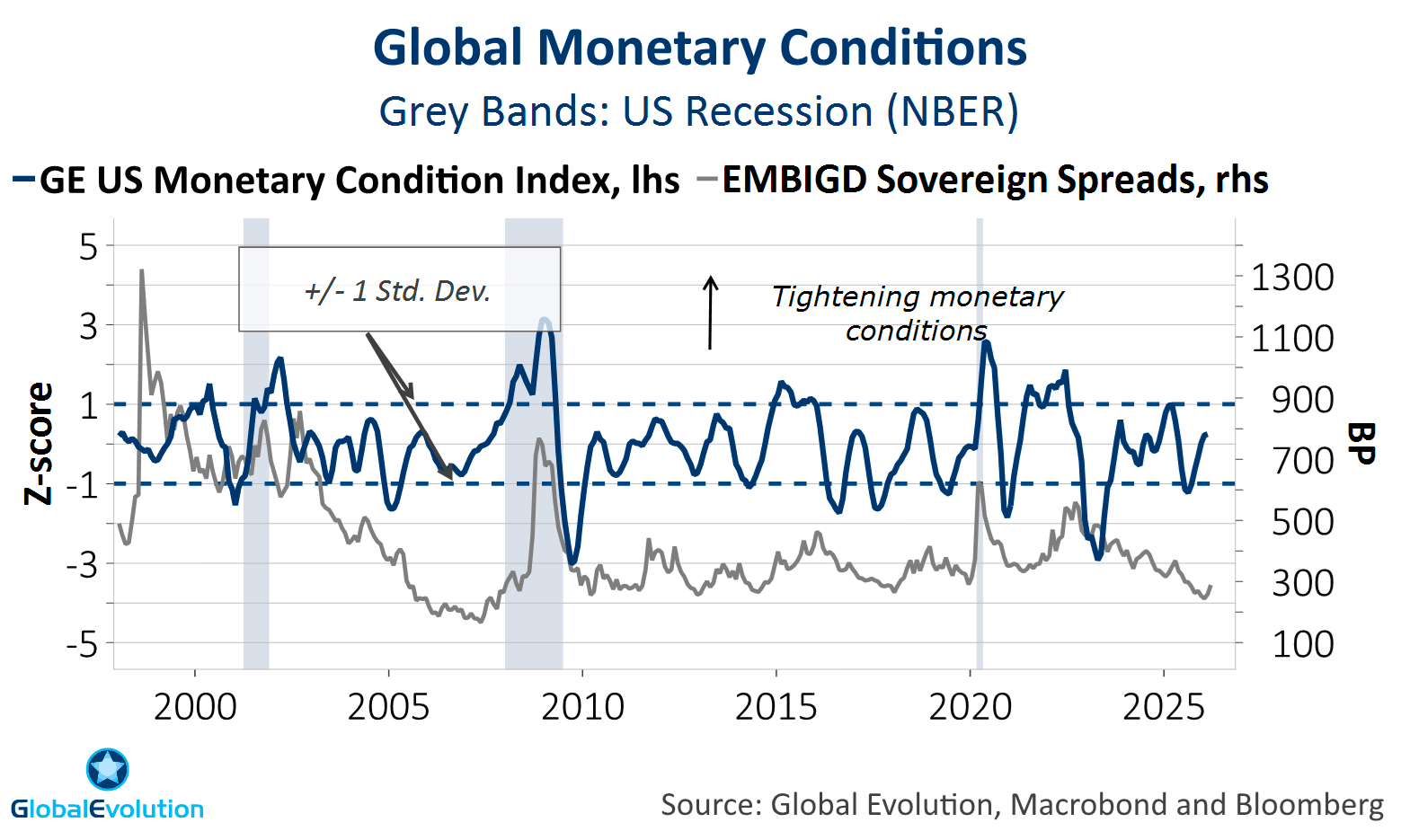

Our expectation of fading monetary tailwinds has been confirmed (LHS), but the pace of tightening is moderating.

Expecting one Fed cut over the coming 12M as growth slows and reaction function becomes more dovish under Warsh.

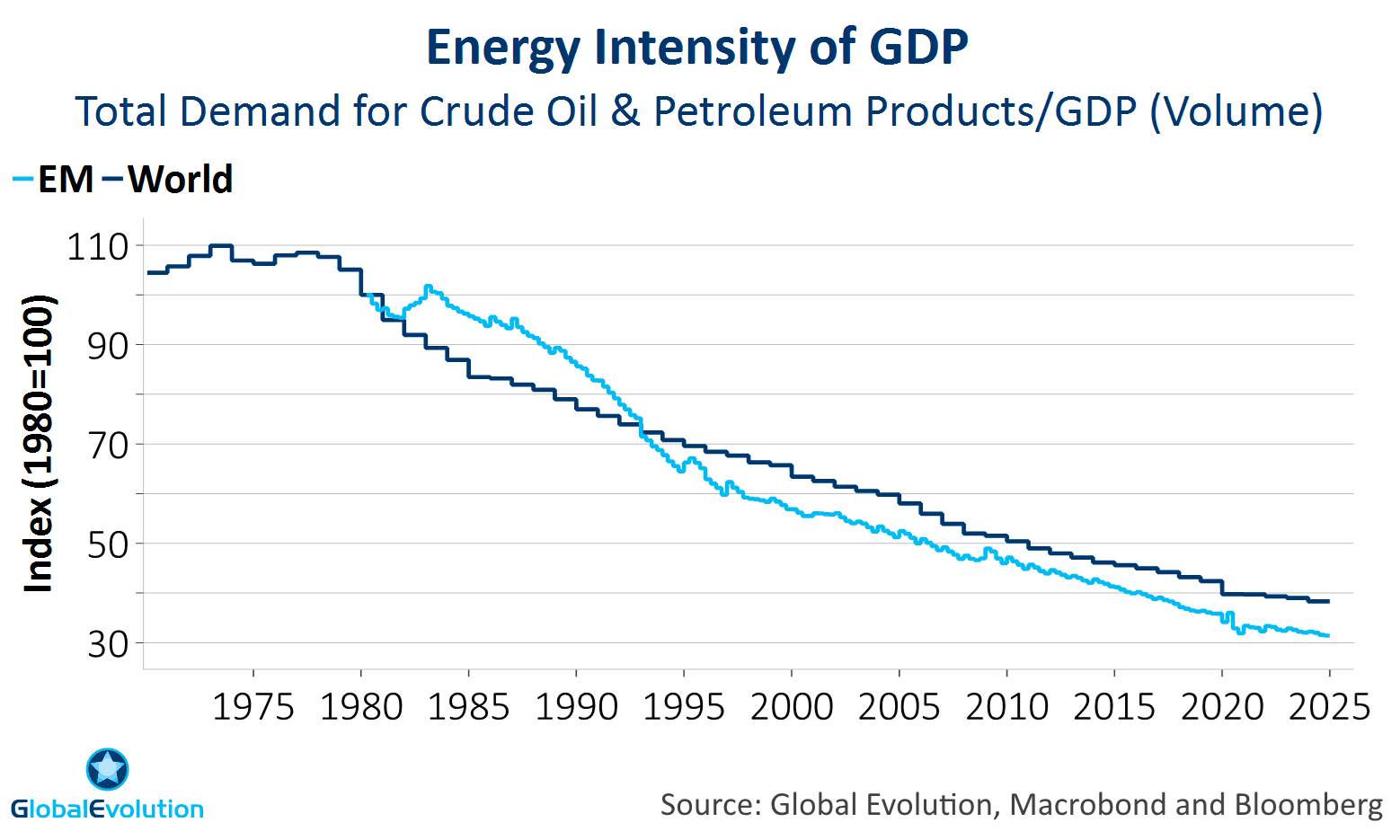

Oil shock NO game changer as energy intensity has declined, both in EM and DM (RHS), and the overall size of the shock is so far less severe than e.g. the Ukraine invasion.

The world has shifted from structural lack of demand in the post-GFC era to a structural lack of supply in the post-Pandemic era.

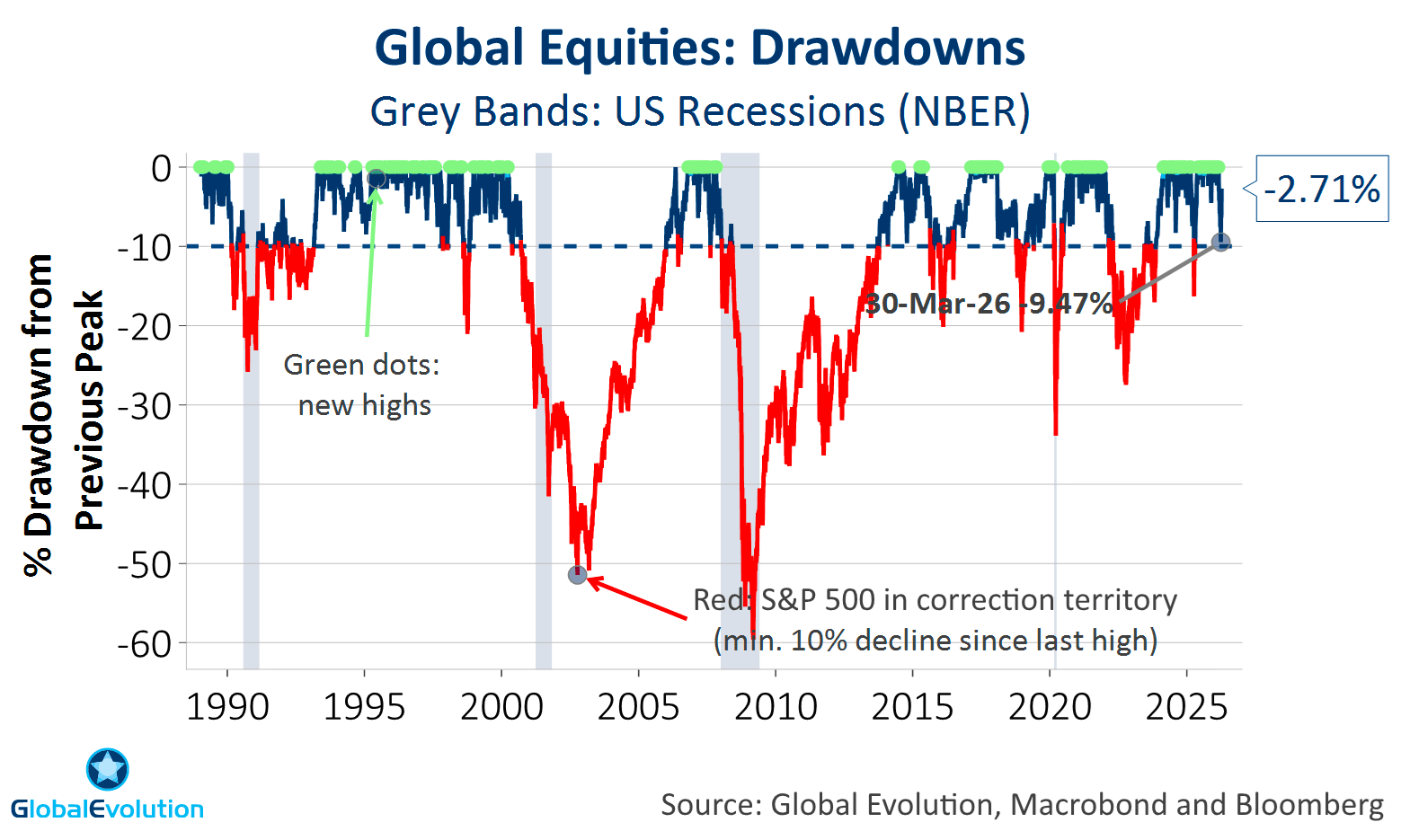

This creates an unstable equilibrium in in macro and markets: Regime shifts towards permantly higher geopolitical, inflation as well as fiscal uncertainty implies a more tactical market environment as market cycles become shorter (LHS).

The dilemma: This calls for diversification when diversification opportunities are drying up.

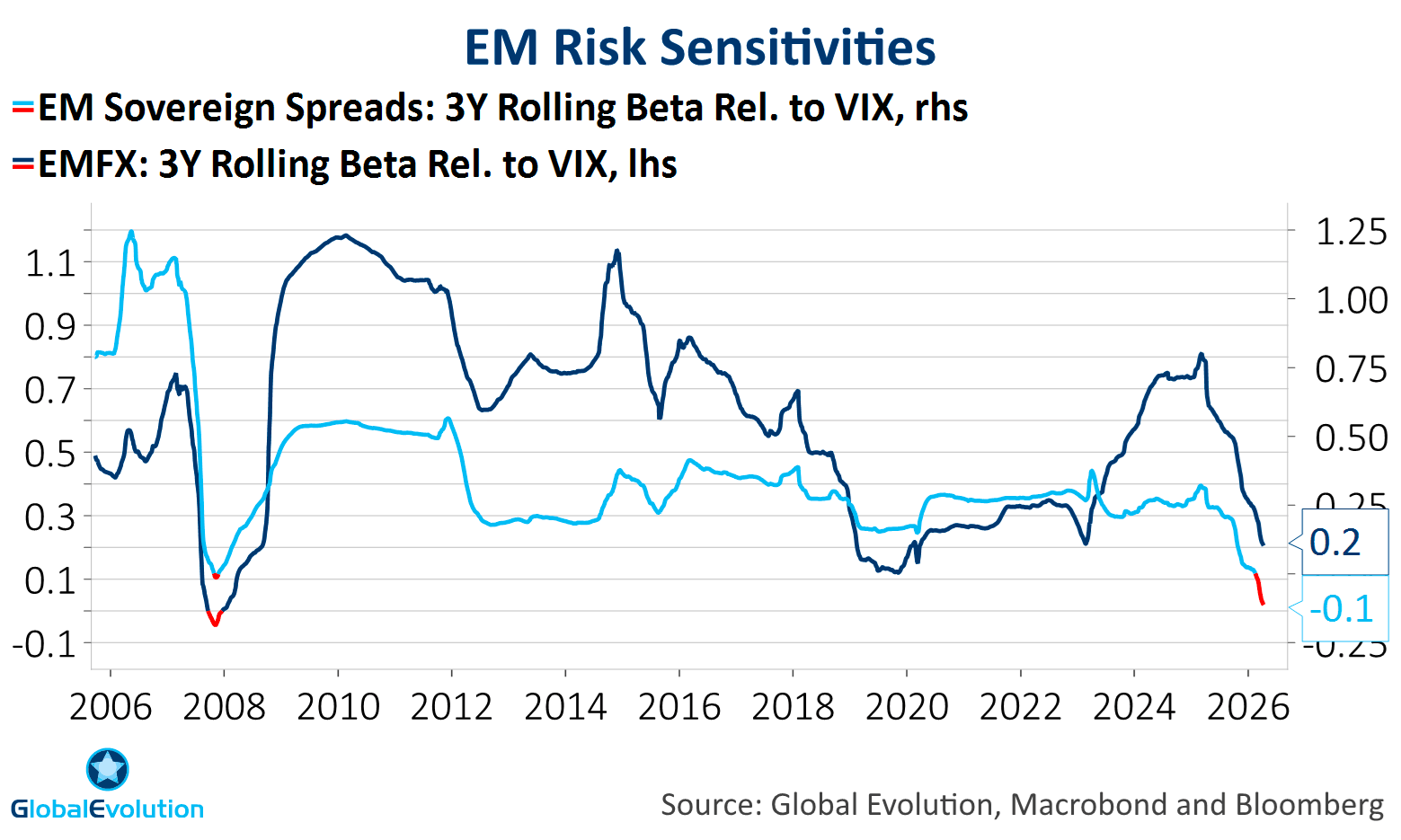

The solution: EMD has been surprisingly resilient – even during the most recent setback as EMD betas to global risk appetite have declined (LHS). This highlights not only EMD’s relative resilience, but also its diversification appeal.

Three signposts to gauge where we are in the sell-off suggest the worst is behind us as a de-escalatory path crystalizes.

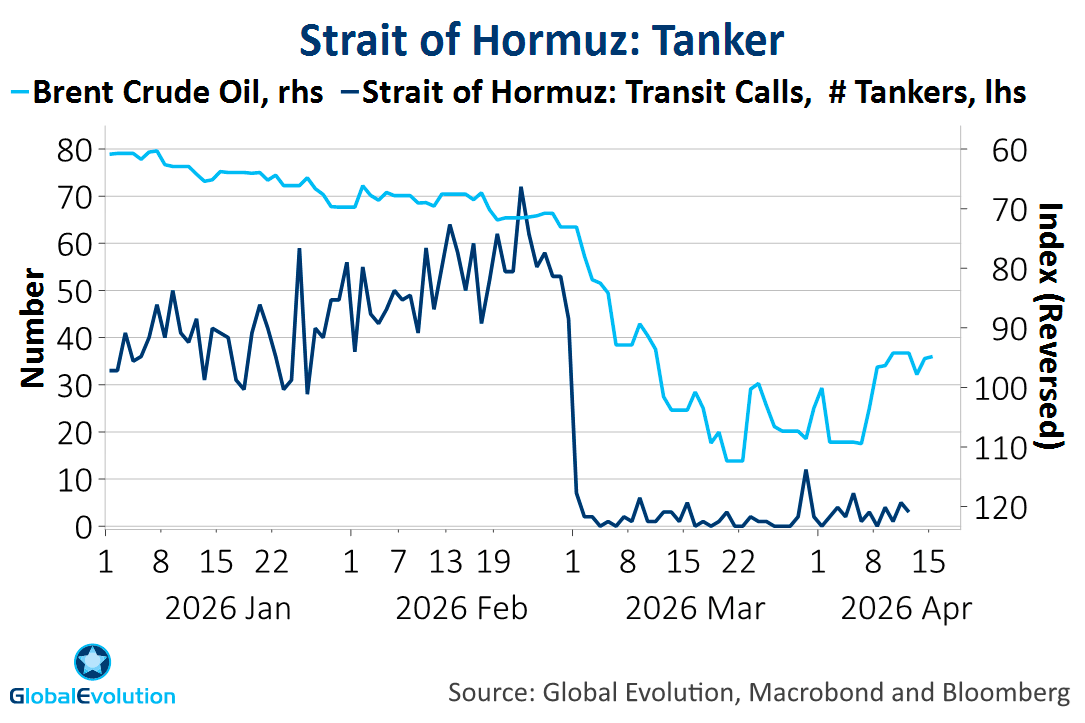

We believe the energy supply disruption has peaked as the number of tankers passing the Strait of Hormuz has bottomed – it’s the delta that matters (LHS).

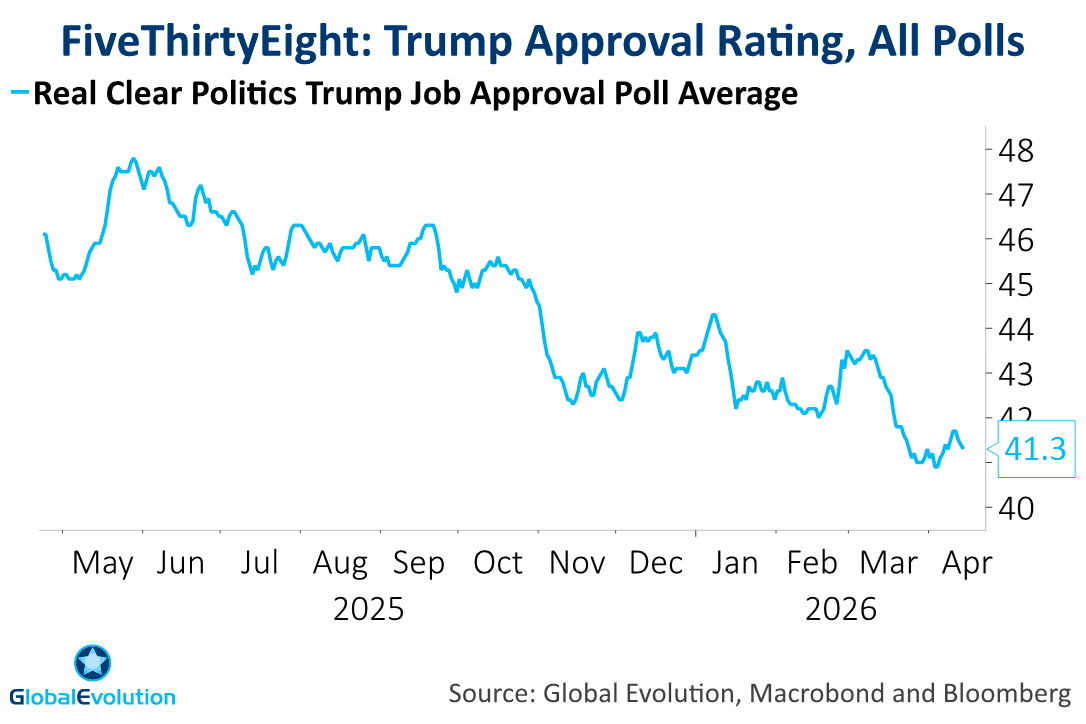

Trump’s approval rating hit new lows (center) → cease fire confirms that the White House is “blinking” & has a desire to de-escalate.

After triggering a risk-off signal earlier in the year, our Risk Index (RHS) is closer to the risk-on threshold than the risk-off threshold.

Bottom-line: In the context of a more tactical market environment as compared to 2025, the set-back in March doesn’t lead to a major repricing of the growth backdrop. Rather, it is an attractive entry point into EMD risk and EM FX risk, in particular.

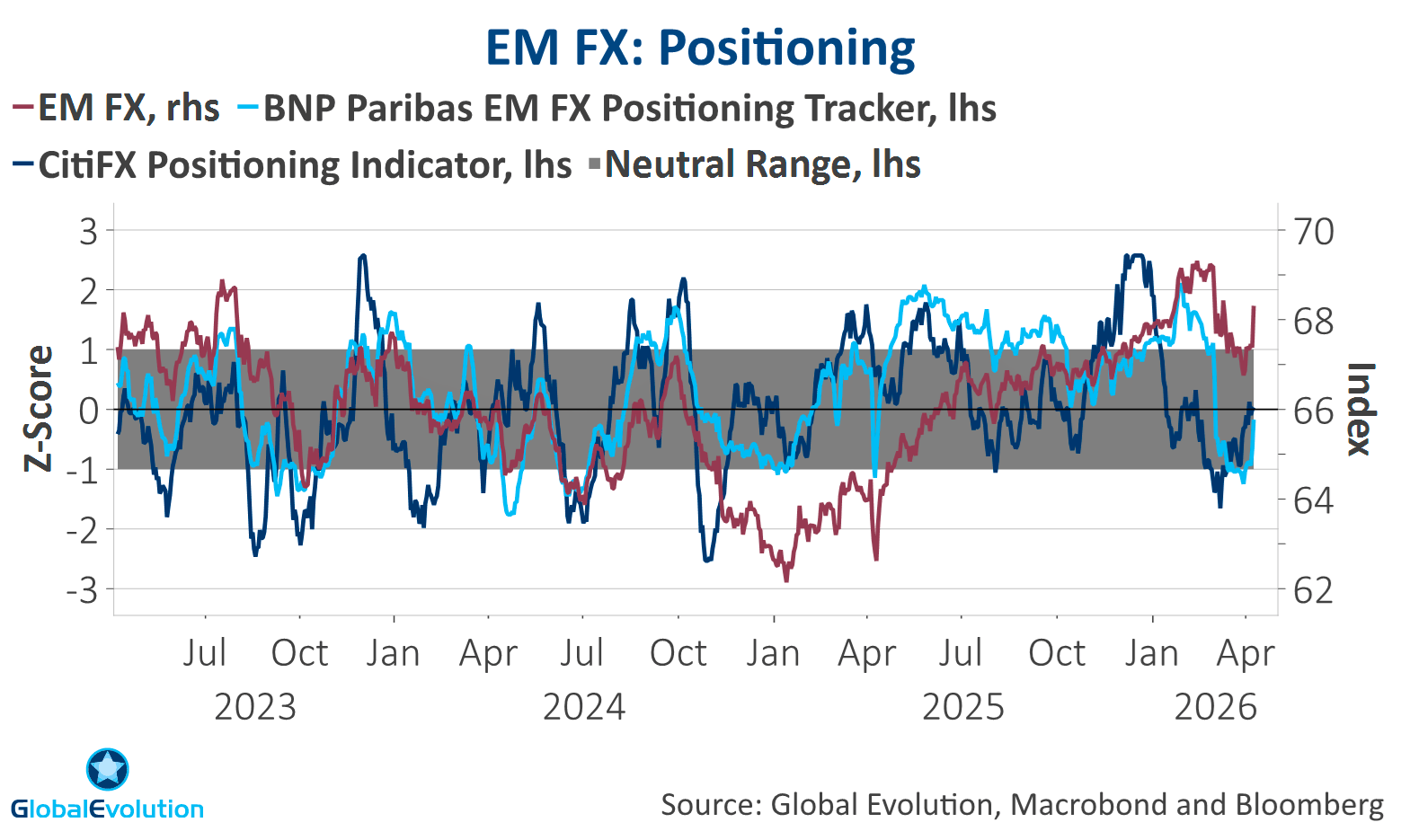

Shifting from U/W EMFX to a tactical overweight. Key drivers: Positioning has reversed from extreme long positioning (LHS), sentiment is more neutral and we see a clearer path towards de-escalation in the Middle East.

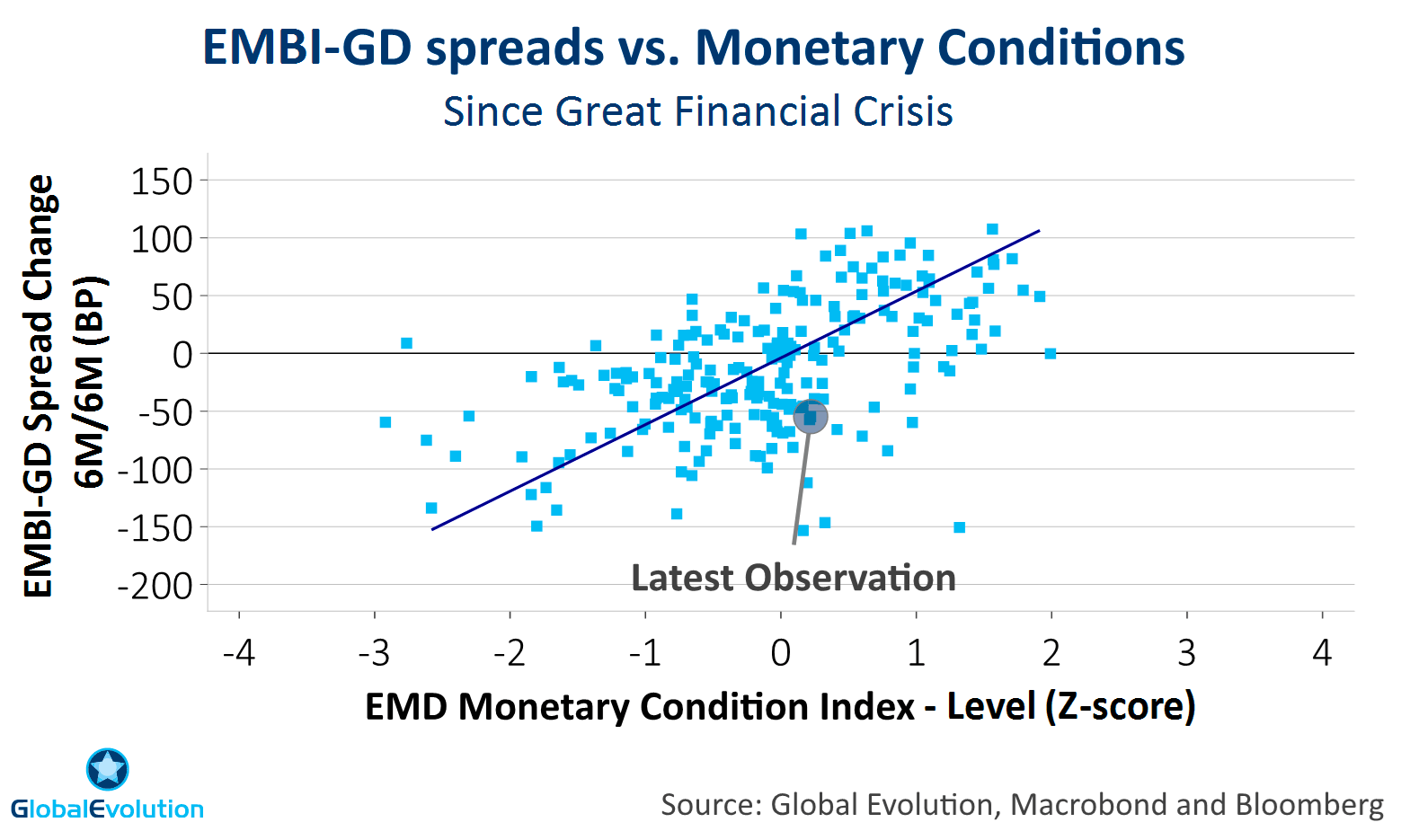

Monetary tightening suggests two-sided risks to spreads at current levels (RHS). Risk-reward in local EMD seem more attractive.

On a 12M horizon, we expect renewed easing, but also softer growth, which should favour hard currency over local currency.

Disclaimer & Important Disclosures

Global Evolution Asset Management A/S (“GEAM”) is incorporated in Denmark and authorized and regulated by the Danish FSA (Finanstilsynet). GEAM DK is located at Buen 11, 2nd Floor, Kolding 6000, Denmark.

GEAM has a United Kingdom branch (“Global Evolution Asset Management A/S (London Branch)”) located at Level 8, 24 Monument Street, London, EC3R 8AJ, United Kingdom. This branch is authorized and regulated by the Financial Conduct Authority under FCA # 954331. In Canada, while GEAM has no physical place of business, it has filed to claim the international dealer exemption and international adviser exemption in Alberta, British Columbia, Ontario, Quebec and Saskatchewan.

In the United States, investment advisory services are offered through Global Evolution USA, LLC (‘Global Evolution USA”), a Securities and Exchange Commission (“SEC”) registered investment advisor. Global Evolution USA is located at: 250 Park Avenue, 15th floor, New York, NY. Global Evolution USA is a wholly owned subsidiary of Global Evolution Financial ApS, the holding company of GEAM. Portfolio management and investment advisory services are provided to GE USA clients by GEAM. GEAM is exempt from SEC registration as a “participating affiliate” of Global Evolution USA as that term is used in relief granted by the staff of the SEC allowing U.S. registered investment advisers to use investment advisory resources of non-U.S. investment adviser affiliates subject to the regulatory supervision of the U.S. registered investment adviser. Registration with the SEC does not imply any level of skill or expertise. Prior to making any investment, an investor should read all disclosure and other documents associated with such investment including Global Evolution’s Form ADV which can be found at https://adviserinfo.sec.gov.

In Singapore, Global Evolution Fund Management Singapore Pte. Ltd (“Global Evolution Singapore”) has a Capital Markets Services license issued by the Monetary Authority of Singapore for fund management activities. It is located at Level 39, Marina Bay Financial Centre Tower 2, 10 Marina Boulevard, Singapore 018983.

GEAM, Global Evolution USA, and Global Evolution Singapore, together with their holding companies, Global Evolution Financial Aps and Global Evolution Holding Aps, make up the Global Evolution group affiliates (“Global Evolution”).

Global Evolution, Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC, and Pearlmark Real Estate, L.L.C. and its subsidiaries are all direct or indirect subsidiaries of Conning Holdings Limited (collectively, “Conning”) which is one of the family of companies whose controlling shareholder is Generali Investments Holding S.p.A. (“GIH”) a company headquartered in Italy. Assicurazioni Generali S.p.A. is the ultimate controlling parent of all GIH subsidiaries. Conning has investment centers in Asia, Europe and North America.

Conning, Inc., Conning Investment Products, Inc., Goodwin Capital Advisers, Inc., Octagon Credit Investors, LLC, PREP Investment Advisers, L.L.C. and Global Evolution USA, LLC are registered with the SEC under the Investment Advisers Act of 1940 and have noticed other jurisdictions they are conducting securities advisory business when required by law. In any other jurisdictions where they have not provided notice and are not exempt or excluded from those laws, they cannot transact business as an investment adviser and may not be able to respond to individual inquiries if the response could potentially lead to a transaction in securities.

Conning, Inc. is also registered with the National Futures Association. Conning Investment Products, Inc. is also registered with the Ontario Securities Commission. Conning Asset Management Limited is Authorised and regulated by the United Kingdom's Financial Conduct Authority (FCA#189316); Conning Asia Pacific Limited is regulated by Hong Kong’s Securities and Futures Commission for Types 1, 4 and 9 regulated activities; Global Evolution Asset Management A/S is regulated by Finanstilsynet (the Danish FSA) (FSA #8193); Global Evolution Asset Management A/S (London Branch) is regulated by the United Kingdom's Financial Conduct Authority (FCA# 954331); Global Evolution Asset Management A/S, Luxembourg branch, registered with the Luxembourg Company Register as the Luxembourg branch(es) of Global Evolution Asset Management A/S under the reference B287058. It is also registered with the CSSF under the license number S00009438.. Conning primarily provides asset management services for third-party assets.

This publication is for informational purposes and is not intended as an offer to purchase any security. Nothing contained in this communication constitutes or forms part of any offer to sell or buy an investment, or any solicitation of such an offer in any jurisdiction in which such offer or solicitation would be unlawful.

All investments entail risk, and you could lose all or a substantial amount of your investment. Past performance is not indicative of future results which may differ materially from past performance. The strategies presented herein invest in foreign securities which involve volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for investments in emerging and frontier markets. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, and credit.

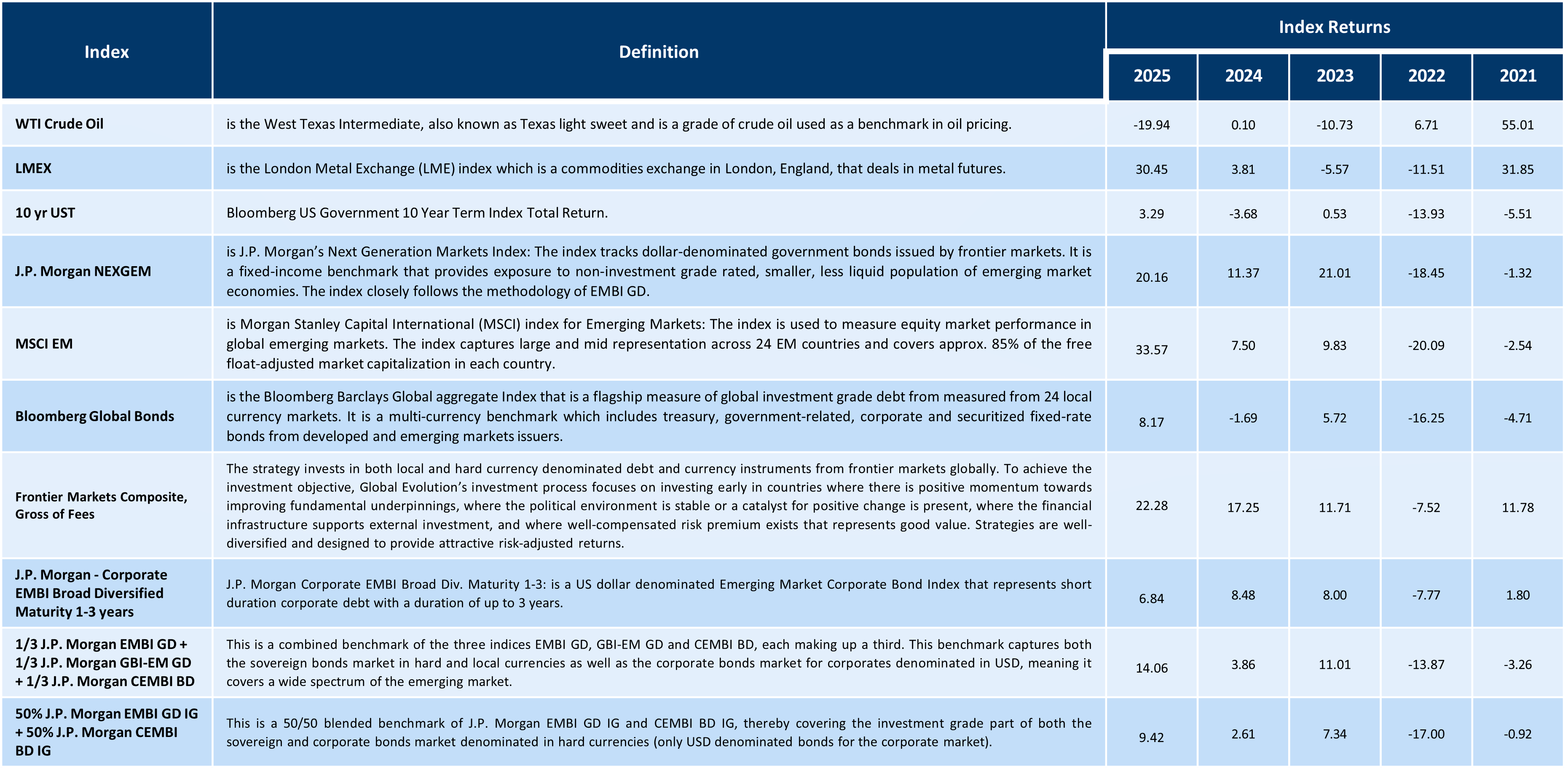

This communication may contain Index data from J.P. Morgan or data derived from such Index data. Index data information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The Index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan's prior written approval. Copyright 2024, J.P. Morgan Chase & Co. All rights reserved.

This communication may contain aggregate peer analysis data has been obtained from eVestment Alliance LLC and its affiliated entities (collectively, "eVestment"). eVestment reserves all rights, including to ownership and distribution. eVestment collects information directly from investment management firms and other sources believed to be reliable; however, eVestment does not guarantee or warrant the accuracy, timeliness, or completeness of the information provided and is not responsible for any errors or omissions. Performance results may be provided with additional disclosures available on eVestment’s systems and other important considerations such as fees that may be applicable. Not for general distribution. * All categories not necessarily included; Totals may not equal 100%. Copyright 2013‐2024 eVestment Alliance, LLC. Returns less than a year are not annualized.

While reasonable care has been taken to ensure that the information herein is factually correct, Global Evolution makes no representation or guarantee as to its accuracy or completeness. The information herein is subject to change without notice. Certain information contained herein has been provided by third party sources which are believed to be reliable, but accuracy and completeness cannot be guaranteed. Global Evolution does not guarantee the accuracy of information obtained from third party/other sources.

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

Legal Disclaimer ©2026 Global Evolution.

This document is copyrighted with all rights reserved. No part of this document may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of Global Evolution, as applicable.

Copyright © 2026 Global Evolution - All rights reserved